Overview

This week's pick is TransDigm Group (TDG), an Ohio-based industrials company that makes highly engineered components for commercial and defense aircraft. About 75% of its revenue comes from proprietary, sole-source parts, meaning airlines and operators have no choice but to buy from TransDigm to keep their planes in the air.

The real engine of the business is the aftermarket. Once a TransDigm part is installed on an aircraft, it must be replaced repeatedly over the plane's lifetime, which can span 20 to 30 years. That locked-in and recurring demand is what drives the company's pricing power, industry-leading margins, and remarkably consistent free cash flow.

Layer in a meaningful defense business backed by long-term government contracts, and it becomes clear that TransDigm is built to perform in almost any environment.

Drivers

1. Pricing Power

One of TransDigm's most durable advantages is its ability to raise prices and get away with it. Since so many of its components are sole-sourced and FAA-certified, switching to a competitor isn't just inconvenient—it's often effectively impossible.

Airlines and defense contractors need these parts constantly, and recertifying an alternative supplier can take years and cost millions of dollars. That dynamic gives TransDigm a level of pricing control rarely seen in manufacturing, which shows up directly in its margins.

2. Acquisitions

The company targets small, niche aerospace suppliers with proprietary products, acquires them at reasonable prices, and then applies its operating playbook to expand margins and unlock value.

It's essentially a private-equity strategy operating inside a public company. The aerospace component market remains highly fragmented, providing a substantial runway for future acquisitions.

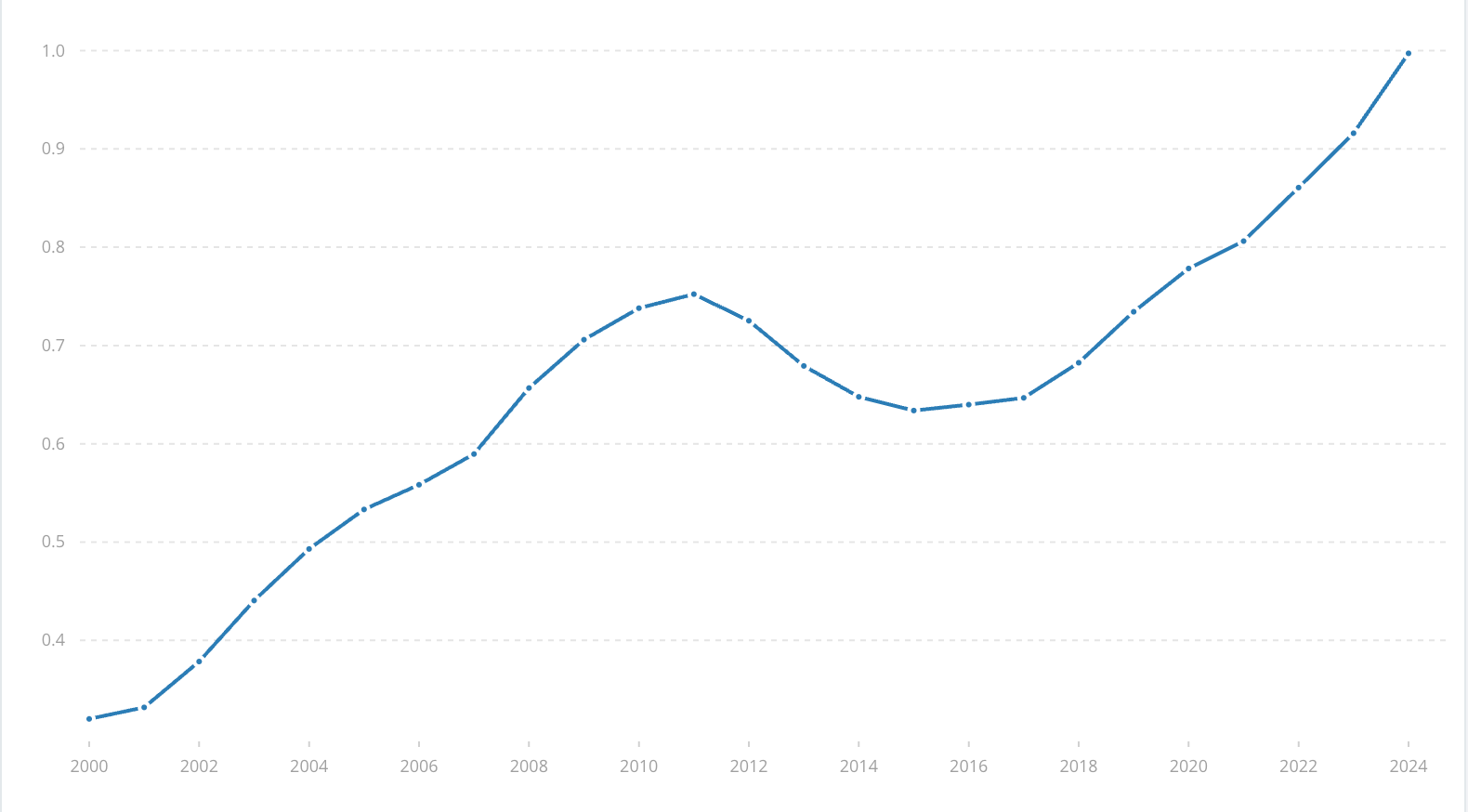

3. Defense Exposure

TransDigm's commercial aerospace business gets most of the attention, but its defense exposure is an important growth engine.

As global defense budgets rise amid increasing geopolitical tensions, countries continue investing in larger and longer-duration military aircraft programs. TransDigm supplies critical components for many of these platforms.

These contracts tend to be long-term and highly recurring, creating a stable revenue stream that helps offset cyclical weakness in commercial aviation.

US Defense Spending ($T) Since 2000

Risks

The primary risk to TransDigm is a downturn in airline demand, which could reduce flight hours and slow replacement cycles.

However, most of the company's profit comes from mission-critical aftermarket parts that must be replaced regardless of new aircraft orders, making revenue more resilient than it might initially appear.

Regulatory scrutiny of pricing is another consideration, though the highly engineered and certified nature of its products limits the availability of substitutes.

The Financials

TransDigm has built one of the strongest financial profiles in the industrial sector.

The company generated nearly $8.8 billion in revenue in its most recent fiscal year, up roughly 11% year over year, and expects revenue to reach approximately $9.75–$9.95 billion in fiscal 2026.

More impressively, TransDigm consistently converts more than half of its revenue into EBITDA, a level of profitability rarely seen among manufacturers.

- Revenue: $8.8 Billion

- Revenue Growth: ~11%

- EBITDA: $4.5 Billion

- Free Cash Flow: $1.8+ Billion

- Capital Returned to Shareholders: $5.8 Billion

Why Buy TDG?

At its core, TransDigm is a business built to win. The company dominates manufacturing highly specialized, difficult-to-replace aerospace components and has spent decades acquiring niche aerospace businesses while generating exceptional returns.

Air travel demand continues to rise globally, aircraft utilization remains strong, and planes require TransDigm's parts to stay operational.

The financials reinforce the story: high margins, consistent double-digit growth, substantial free cash flow generation, and billions returned to shareholders.

For long-term investors, TDG offers a rare combination of defensive characteristics and growth potential. In an uncertain market environment, TransDigm remains one of the highest-quality aerospace businesses available.

Disclaimer: This article is for informational and educational purposes only and should not be considered investment advice. Always conduct your own research before making investment decisions.