The Business Behind Starbucks

When Brian Niccol took over the reins as CEO of Starbucks in September 2024, the company was in free fall. During the tumultuous 17-month tenureship of his predecessor, Laxman Narasimhan, Starbucks lost nearly $30 billion in market value due to declining sales in its two largest markets (the US and China), operational challenges, long wait times, and a deteriorating customer experience (Medium). In response, the board turned to Niccol, a proven turnaround specialist, who had prior success at Chipotle, to stabilize the business, and early signs suggest progress. In its last earnings report, Starbucks reported revenue growth of 6% and US same-store sales growth of 4% (WSJ).

But what has actually changed, and more importantly, what business is Starbucks really in?

At its core, Starbucks operates a simple business model: sell low-cost products at premium prices by elevating the customer experience. Unlike traditional franchise models, in which a company hires an independent operator to run the stores, Starbucks owns a majority of its locations. Owning approximately 58% of its stores, Starbucks controls everything from store design to service standards, an advantage that allows the company to deliver a consistent premium experience across locations (Forbes). This business model gives Starbucks more control and higher potential margins, but also exposes it to higher operating costs and execution risk.

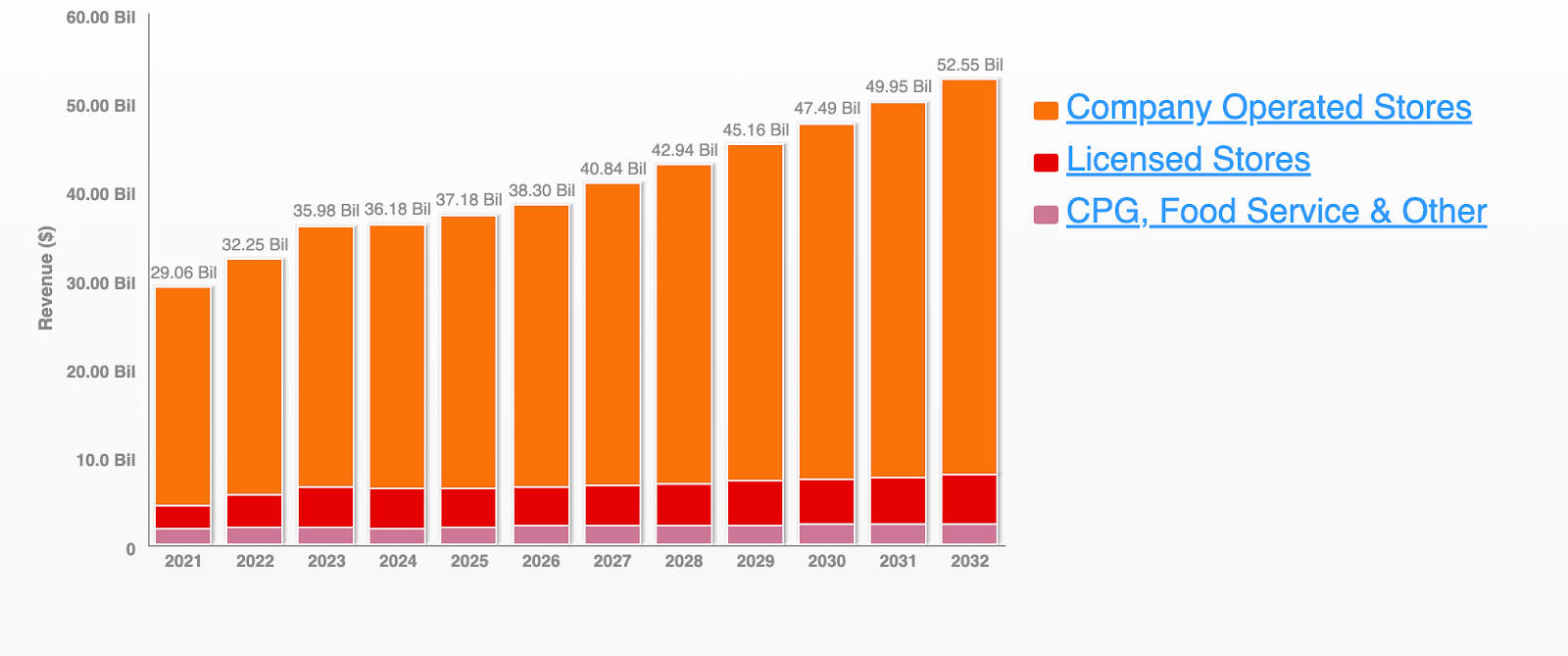

Source: Trefis Analysis of Starbucks Revenue

The company's revenue breakdown highlights the importance of this model. While company-operated stores account for just over half of total locations, they generate 82.7% of revenue in 2025 (Trefis). Licensed stores contribute 11.7%, with the remaining 5.6% coming from consumer packaged goods, food service, and other segments (Trefis). In other words, Starbucks prioritizes ownership over scale because it can capitalize on higher margins while absorbing the high costs of labor, rent, and operations.

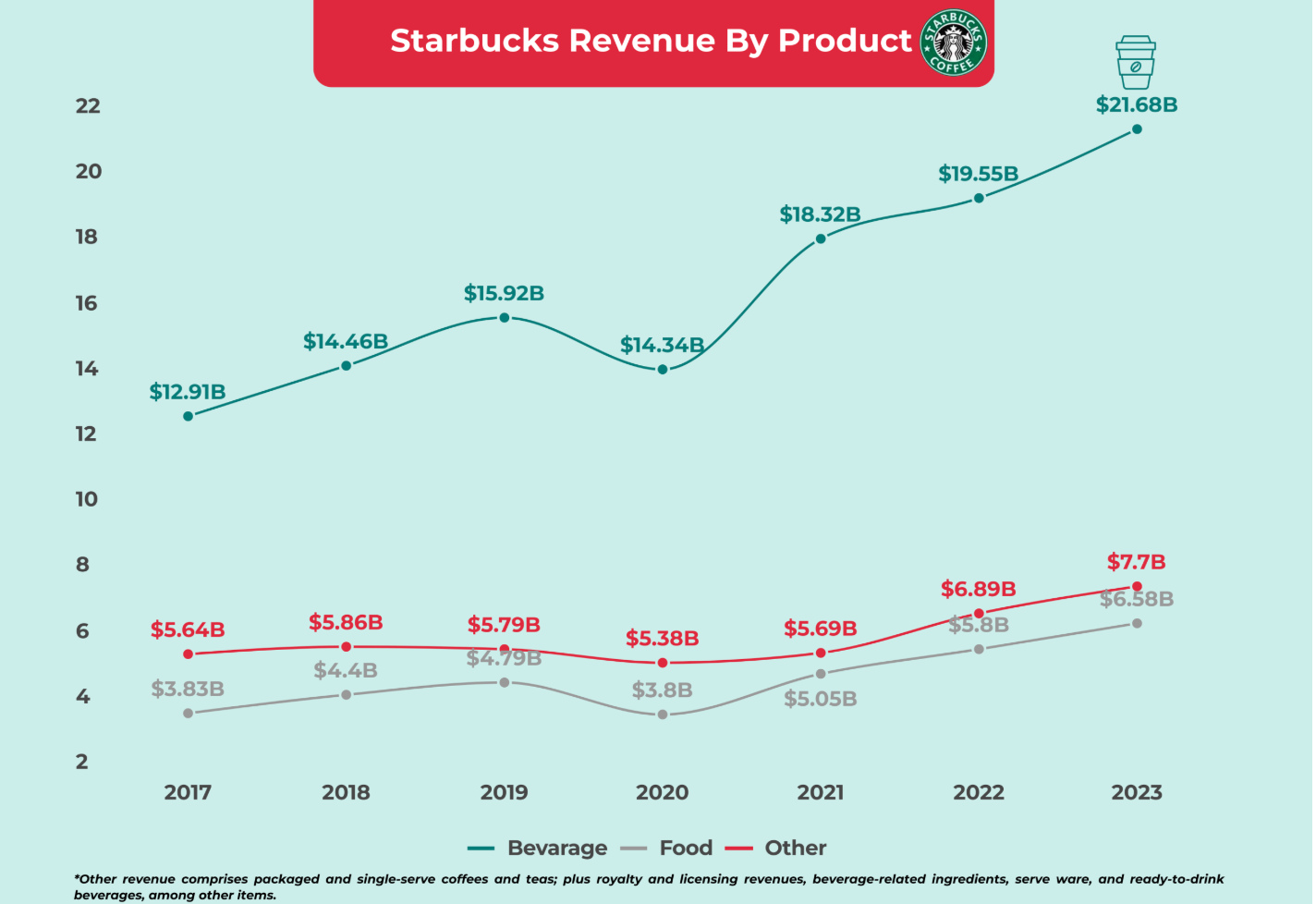

Source: FourWeekMBA Starbucks Revenue By Product

A closer look at revenue by product reveals that beverages account for the majority of revenue, a position Starbucks leans into. Across the industry, drinks carry higher profit margins than food, as Starbucks uses customization, consistency, and brand recognition to charge higher prices for its drinks. Unlike its competitors, McDonald’s or Tim Hortons, customers at Starbucks are willing to pay $5-$7 for these premium beverages, not because of the underlying product cost, but because of the perceived value attached to the brand. Starbucks’ pricing power stems less from the quality of the coffee itself and more from what surrounds it.

Under Niccol, Starbucks quickly launched its “Back to Starbucks” strategy, aimed at restoring growth by refocusing on its core identity, a community-centered coffeehouse. The plan emphasizes improving store operations, strengthening the brand, and reestablishing Starbucks’ presence as the community coffeehouse (Starbucks Corporation). This strategic repositioning shifts the company's direction back towards its original vision. Starbucks is not just a place to buy coffee, but a third place between home and work where customers can spend time, grab some coffee and a bite to eat, relax, and do some work in the mornings. Store design, seating, and ambiance all play a crucial role in reinforcing this position, and Starbucks is willing to improve its stores, planning to spend hundreds of millions on capital expenditures to enhance its locations (WSJ).

However, this renewed focus creates tension with Starbucks’ recent growth strategy. Investments in mobile ordering and operational efficiency have improved speed and convenience, but often at the expense of the in-store experience. As Starbucks scaled in the 2010s, it faced an inherent trade-off: growing into a $100 billion company required sacrificing the small-boutique coffee-shop experience that originally defined the brand (WSJ). The challenge now facing Starbucks is managing this delicate balance, maintaining an experience that justifies its premium pricing while continuing to operate at scale.

To close out the article, I will provide a SWOT analysis of Starbucks to evaluate the company’s position by identifying internal strengths and weaknesses, as well as external opportunities and threats.

Strengths:

Strong Brand Recognition

Pricing Power

Strong Digital Presence.

Weaknesses

Owned Stores Can Create Large Operating Costs

Dependence on Single Product (Coffee)

Expensive Products

Opportunities

Further Global Expansion

Partnerships and Collaborations With Other Brands

Bolster Online Channels

Threats

Coffee Beans Price Volatility

Labor Disputes and Employee Turnover

Competition from Other Coffee Chains and Independent Coffee Shops.