The Illusion of Strength: A Fragile U.S. Economy

At first glance, the US economy appears remarkably resilient. Job growth remains solid, consumer spending has held up, and the country has avoided a recession despite high interest rates and persistent inflation. Yet beneath these indicators lies a more fragile reality. A closer look at consumer momentum, labor market trends, and financial conditions suggests that the current expansion may be increasingly unsustainable.

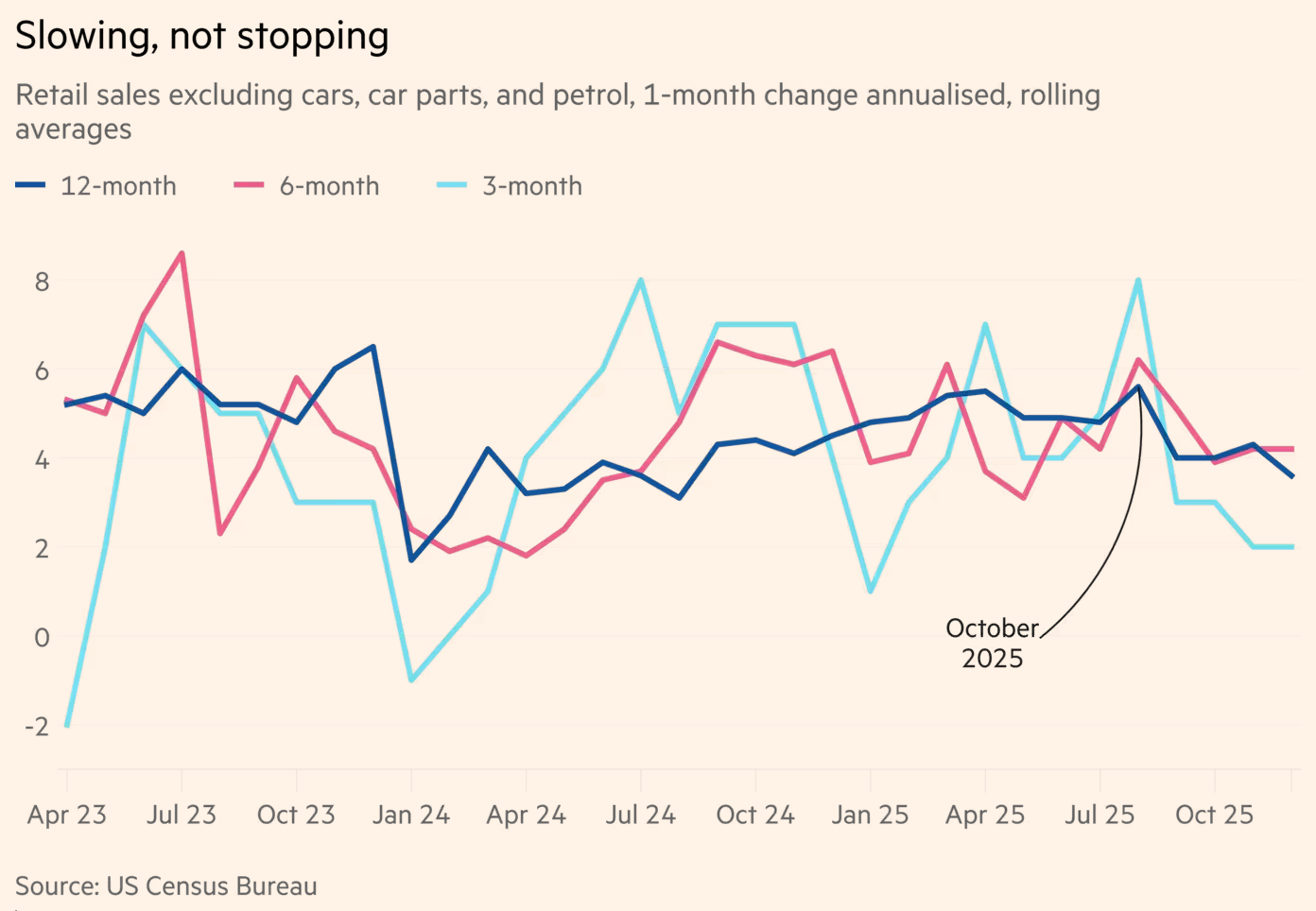

The strength of the US economy has long depended on consumers, who account for roughly two-thirds of economic activity. For several years, consumption has continued to expand despite “persistent inflation, assorted geopolitical shocks and terrible consumer sentiment” (FT). However, recent data suggests that this resilience may be fading. Retail sales growth was flat at the end of 2025, and broader measures of spending declined slightly. While the slowdown is not dramatic, it is widespread. Evidence shows that consumer momentum peaked in October and has clearly weakened since then, raising concerns about whether consumers can continue to drive economic growth at the same pace.

The apparent stability of consumer spending masks significant underlying disparities. Higher-income households, who experienced large gains in the stock market last year, have continued to spend at relatively high levels (WSJ). Many higher-income households have more fuel-efficient cars, making them less sensitive to increases in gas prices. In contrast, lower and middle-income households are facing growing financial strain. Credit card and auto loan delinquency rates for these groups now exceed their pre-pandemic peak. At the same time, the personal savings rate has fallen sharply, reaching its lowest level since 2008, excluding the pandemic (FT).

Even among wealthier households, there are emerging signs of weakness. Consumer sentiment declined by 6% in March to 53.3, below the projected 54.2, with higher-income consumers reporting particularly large drops in confidence due to rising gas prices and declining stock market performance (CNN Business). Because affluent households are more sensitive to fluctuations in asset prices, a stock market downturn could significantly reduce their spending. Recent consumption strength has been heavily reliant on higher-income consumers, and if their spending slows, the entire economy may follow.

Recent economic data reinforces the notion that current conditions are more fragile than they seem. Retail sales rose by 0.6% in February, marking the strongest increase in seven months, but a closer look reveals that much of this growth was driven by temporary factors (Reuters). Higher gas and supermarket prices contributed significantly to the increase, along with tax refunds, which boosted short-run disposable income for many Americans. Therefore, this recent strength is likely overstated and is unfeasible for the future.

Meanwhile, consumer confidence data presents a mixed yet worrisome picture. Although confidence rose slightly in March, households remain pessimistic about the labor market and anticipate higher inflation in the near future. The underlying labor market indicators are more troubling: hiring and job openings have fallen to their lowest levels since March 2020. While current employment levels remain stable, job creation is slowing, which may weaken income growth and reduce consumer spending.

The labor market itself illustrates the larger theme of an economy that appears strong on the surface but shows signs of underlying weakness. Job growth recovered in March, with payrolls increasing by 178,000, the largest gain since Trump took office last January. However, much of this growth was concentrated in specific sectors such as healthcare, as workers returned following a strike. Other sectors, however, including the federal government and financial services, experienced job losses. Perhaps most concerning is that the labor force participation rate declined to 61.9%, the lowest level since nearly four and a half years. This decrease suggests that fewer people are actively looking for work, which makes the unemployment rate appear lower than it actually is. Additionally, wage growth increased at its slowest pace in almost five years, limiting gains in real income and further constraining consumer spending.

Taken together, these developments point to an economy that remains stable for now but is progressively more vulnerable to shocks. Some economists have described the current environment as a “rolling recession,” in which individual sectors experience recessions independently of one another, while others boom (CNN Business). Others point to a K-shaped theory, where higher-income households’ continued spending keeps the economy afloat. Both frameworks highlight the same underlying issue: the economy’s strength is uneven and dependent on conditions that may not persist.

While a recession is not inevitable, the risks of one are growing. The economy has held up well in recent years, but its foundation appears to be narrowing. Consumer spending is slowing, financial pressures are rising, and signs of weakness are emerging in the labor market. If these trends continue, the current expansion could weaken more rapidly than expected. What appears to be strength today may, in fact, represent the early stages of a more serious slowdown.