CFR’s Portfolio: Bi-Monthly Review

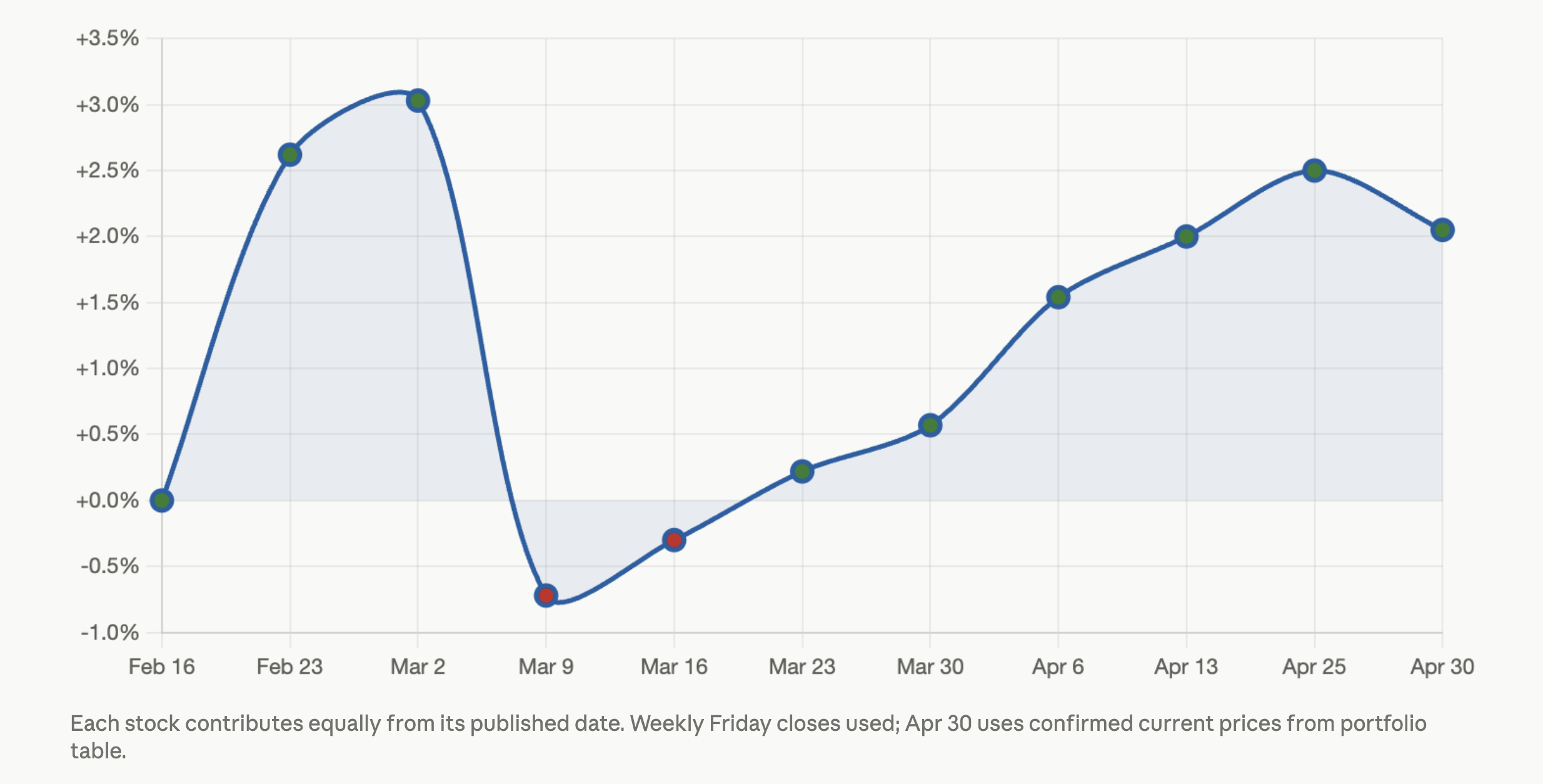

It has now been two months since the inception of CFR’s portfolio, and early returns are somewhat encouraging, given how whiplashed markets have been amid geopolitical tensions, rising inflation, earnings reports, and big market moves. We believe the portfolio has performed relatively well, with some serious winners and, of course, some losers.

Please note that this article was written on the morning of April 30th — markets and stocks are subject to change

Our Investing Approach

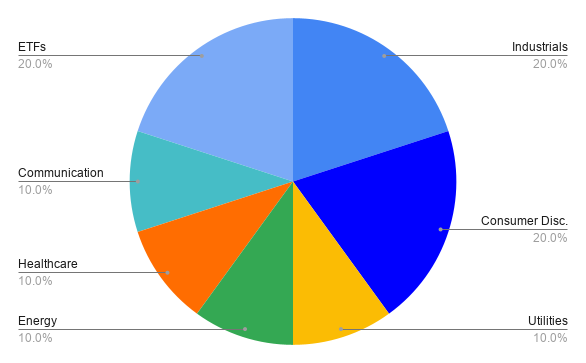

When picking a stock every week, our first thought is always diversification. We want our portfolio to be spread across many sectors to avoid putting all our eggs in one basket. Tailwinds are also considered, as is market sentiment. One of the biggest tailwinds we’ve worked off of is the AI boom and the drive for data center development, which has led us to make picks like NVT and UBER. The overall craze over data centers has also led to the pick of utilities like BEPC.

Beyond individual companies, we focused on mitigating risk and helping the portfolio continue to generate cash, even when the market was down. We scooped up two ETFs: VYM for overall market representation and high dividends, and VWO for emerging-market representation. At the end of the day, the picks we are making are a combination of personal opinion amongst our investment strategy team and our growing understanding of the market and investment strategy. While it would be awesome to boast a +20% return so far on our portfolio, that number is unrealistic for a diversified, risk-managed portfolio over a two-month window — and frankly, not what we are optimizing for.

What’s Up

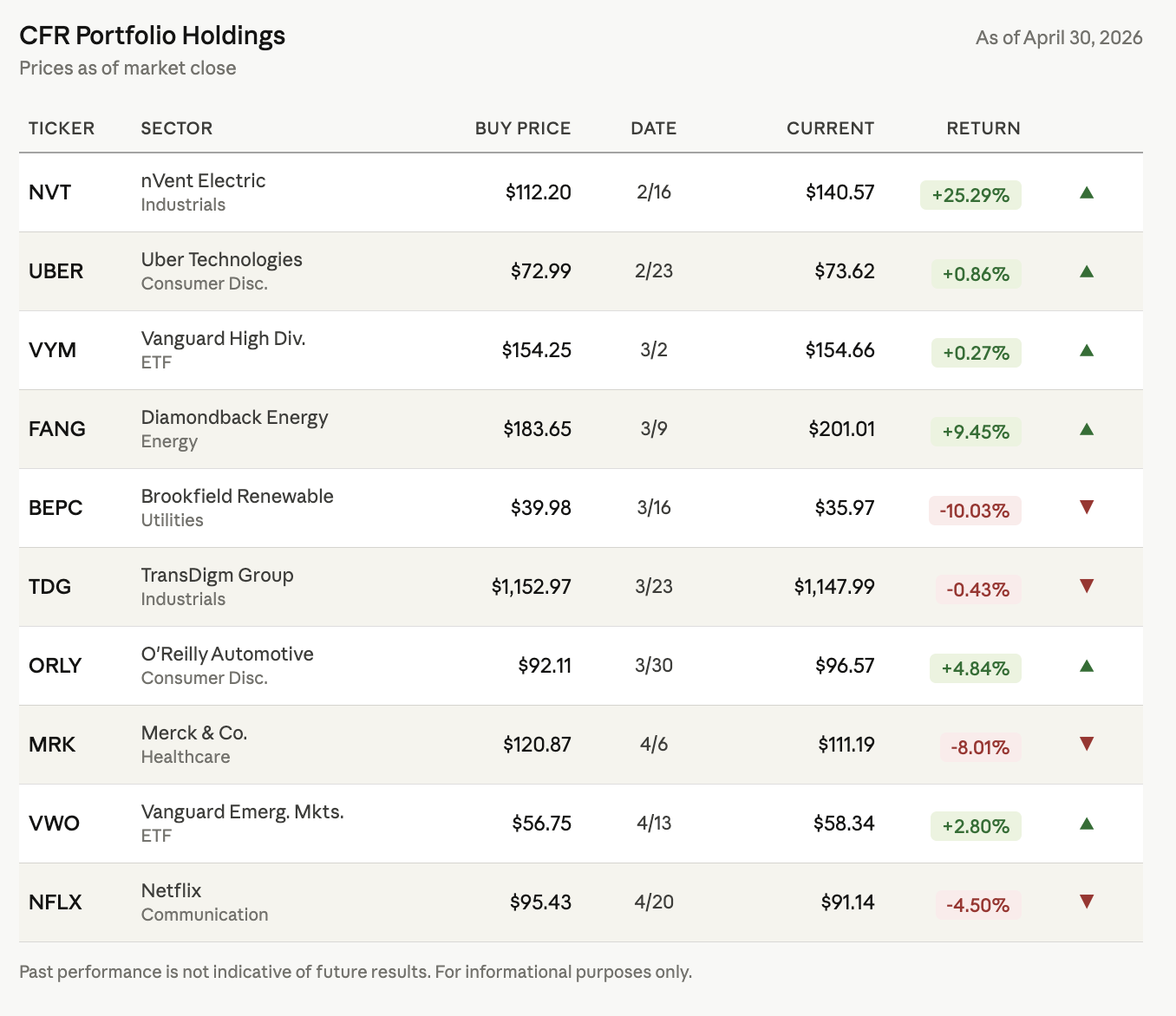

NVT: nVent has seen a massive surge since it was pitched in February, up roughly 25%. The performance can be attributed to its dominance in the world of AI data center infrastructure through its electrical connections, protection, and cooling solutions, as well as to the ever-growing global demand for data centers.

FANG: Diamondback Energy has performed well to date since it was pitched in March, up 11%. This rally can be attributed mainly to the conflict in the Middle East and the whiplashing price of Brent Oil, which has given domestic WTI Oil a steady advantage.

ORLY: O’Reilly Automotive's recent 7% upward performance since it was pitched has been driven by very strong Q1 2026 earnings that outperformed analyst estimates. The consumer is resilient! ORLY is also benefiting from higher interest rates and elevated car prices, which are causing people to turn away from buying new vehicles and focus on fixing their current ones.

VWO: The emerging markets ETF hit a new 52-week high of $59.29 on April 17th, and is up 2.5% since it was pitched 4 days earlier on April 13th. With VWO being heavily weighted in Asian tech giants such as Taiwan Semiconductor (TSMC) and Samsung, the current optimism around AI and data centers has pushed these holdings higher. (Note: VWO is disproportionately benefiting from larger holdings in these companies compared to other broader global funds)

What’s Down

BEPC: Brookfield Renewable Energy has been pressured by a "higher for longer" rate environment (renewable energy utilities like Brookfield need rate cuts to re-rate meaningfully), and Powell holding steady yesterday confirmed that relief isn't coming anytime soon.

MRK: Merck & Co is dealing with Keytruda patent cliff anxiety and a broader rotation out of defensives amid risk-on moments in the market. The stock also got caught in a wave of selling in the pharma sector, tied to concerns about drug pricing policy in Washington.

NFLX: Netflix pulled back after a strong run, entering near $95. Its post-earnings drop is weighing on the position, with disappointing Q2 guidance and Reed Hastings' board departure overshadowing otherwise strong metrics. That said, Q1 beat on both revenue and EPS, and the company authorized a $25 billion buyback – we view the pullback as a potential opportunity rather than a structural concern.

Non-Movers

VYM: VYM is an ETF, designed to be boring, so the fact that it hasn’t budged much (+1% since 3/2) is no surprise. It tracks HY dividend stocks that are largely defensive, staying relatively consistent regardless of the overall economy's state, so there is not much torque in either direction. We bought VYM at fair value, and it has been continuously generating dividend income for us, which the overall P&L does not recognize.

TDG: TransDigm is a steady compounder, but it's not a momentum name, like Boeing. It is a company that has grown over the years through pricing power and acquisitions, not on short-term catalysts. We’ve only held it for a few weeks, which isn't nearly enough time for the thesis to play out. The value here lies in the long term, not a five-week window.

Looking Ahead

Looking ahead, we remain cautiously optimistic on equities. In Powell’s last stand as Fed Chair, he decided to hold rates steady (on 4/29), signaling a higher-for-longer environment, which favors quality companies with strong free cash flow over speculative growth names; a dynamic that supports many of our current holdings.

The consumer has proven more resilient than many anticipated, providing a solid demand backdrop, particularly for our consumer discretionary positions. Q1 earnings have broadly surprised to the upside across major companies, reinforcing that corporate fundamentals remain intact despite macro uncertainty.

The ongoing US-Iran conflict remains a key variable we are watching closely — elevated geopolitical risk has pushed oil prices higher, which acts as a direct tailwind for our energy position in FANG while simultaneously adding inflationary pressure that complicates the Fed's path forward.

On the international side, Brazil has been flagged: with the EWZ (Brazil’s major ETF) up over 20% YTD on EM inflows and dollar weakness, with room to run. As a net oil exporter, Brazil benefits directly from ongoing energy disruptions, and with rates at 14.5%, there is significant room to cut. We have exposure through VWO, but will be on the lookout for more.

Going forward, our approach will prioritize high-quality businesses with durable earnings, while remaining selective about where we add risk in a market that still has meaningful uncertainty around the rate path and geopolitical developments.

Disclaimer: The content published by The Colby Financial Review is for informational and educational purposes only and should not be construed as financial, investment, or trading advice. The views expressed are those of the student authors and do not reflect the views of Colby College or any affiliated institution. Readers should conduct their own research and consult with a qualified financial professional before making any investment decisions.