Introduction

Rather than suggest a pick for this week, we thought it’d be better to take a step back and look at how the market has been moving over the past few months. Since the CFR team left campus in mid-May, a lot has happened in the equities market, some of it expected and some of it very unexpected. I do want to note that there might be a fair bit of hindsight bias in this article. Predicting where the market is going takes immense knowledge and experience; even the best traders often get it very wrong. This article is not to claim that we “knew” what was going to happen, but rather to connect the historical and economic dots to explain why things did and didn’t happen.

The Expected

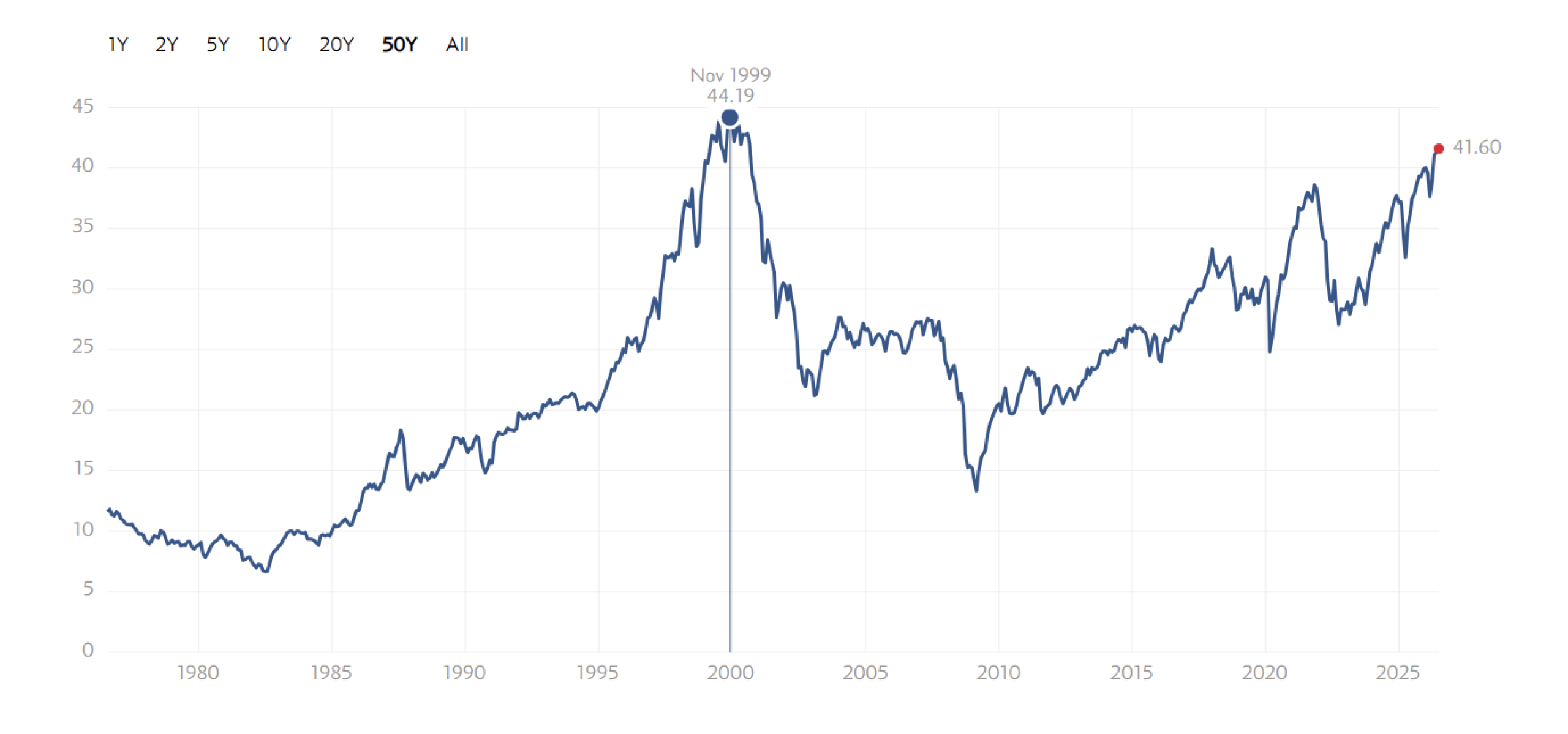

Much of this year’s price action aligns with patterns seen in previous cycles. The most notable is the AI capital expenditure boom and the small-cap value rotation. Even with the steep sell-off in early June, semiconductors have continued to lead the charge, with the Philadelphia Stock Exchange Semiconductor Index (SOX), the benchmark for semiconductors, gaining more than 20% in May and 70% since its March lows at the start of the conflict in the Middle East. The AI infrastructure trade is now on a three-year run, making it unavoidable to compare it to the dot-com bubble. On valuation alone, the Shiller Cyclically Adjusted P/E ratio reached 41.6 in May, the second-highest reading in 140 years of market history, just behind a peak of 44.19 in November of 1999. Fortunately, valuation isn’t the only thing to consider, and while the market does seem a bit bubbly, it is important to note that the dot-com bubble was buoyed by narrative and user growth rather than profits. The S&P 500’s operating margins are near an all-time high of roughly 16%, as profits are rising faster than revenue. This cash flow backing is the strongest argument for why this cycle is different from 1999, even though it shares structural similarities. Just because we won’t see a pop, doesn’t mean there won’t be more of a pullback away from hard-to-believe valuations. As mentioned in our AVUV pick from a few weeks ago, we are starting to see a rotation into small-cap value stocks. The Russell 2000 value index has climbed roughly 23% YTD and is currently outperforming the S&P 500. The emphasis in cash-flow-heavy names within the Financial and Industrial sectors, for example, is similar to the rotation out of mega-caps following the 2000 unwind and the 2021-2022 stretch when rising interest rates pushed investors toward profitability rather than growth.

The Unexpected

The biggest unexpected moment was Oil. Now I don’t mean the conflict itself, but rather how it didn’t hand the US stagflation on a platter. With the oil supply in the Middle East choked off for roughly 5 months, many analysts believed the situation would drive inflation higher, crush growth, and cause wages to stagnate, similar to what the economy faced in 1973 during the Organization of Arab Petroleum Exporting Countries (OPEC) oil crisis. However, while inflation ticked up to 3.8% YoY in April CPI, the market seemingly didn’t care, with no wage spiral and the economy growing at a steady pace. Both of these factors were held up by strong corporate earnings and resilient labor markets, with April payrolls, for example, rising by 115,000 versus expectations of roughly 60,000. One of the most notable data points was the University of Michigan’s Consumer Sentiment Index reaching an all-time record low of 44.8 in May. In the same period, equities continued to set new record highs, showing how consumer sentiment can capture how people feel about the economy in the moment, while market prices reflect what’s expected going forward. So far, the market’s economic read this year has been right.