The Return of the Oil Shock

For most of the past year, it seemed like the US economy was finally recovering from the extreme inflation that followed the pandemic. Inflation had fallen significantly from its 2022 peak, and many investors believed the Fed would begin cutting interest rates this year. That all changed in February, when the US and Israel launched attacks on Iran, disrupting energy markets and causing oil prices to soar. As disruptions in the Strait of Hormuz continue to threaten global energy supplies, economists are becoming more concerned about stagflation: the combination of high inflation and weak economic growth.

Oil prices have risen sharply since the conflict began in early 2026. Brent crude prices are now more than 65% above pre-war levels, and some economists are warning that oil prices could climb even higher. Citi estimates that if oil reaches $120 per barrel through the end of the year, global growth could fall significantly, while inflation could hit 5%. Economists have compared these fears to the 1970s energy crisis, when conflict in the Middle East pushed many advanced economies into years of economic instability.

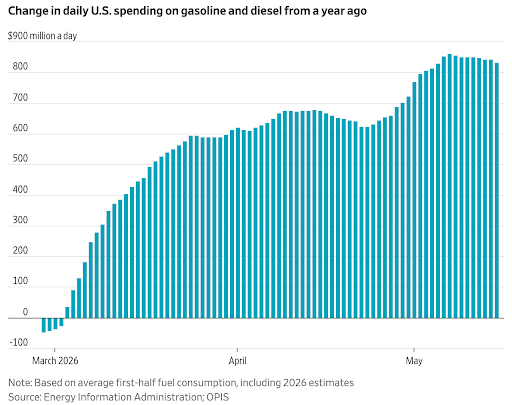

Oil shocks affect almost every part of the economy, raising transportation costs, increasing production costs for businesses, and making shipping more expensive. These higher costs eventually reach consumers and affect their behavior. In March, for example, airlines spent almost $1.3 billion more on jet fuel than they did the previous year. JPMorgan estimates that if gas prices remain elevated through 2026, Americans could spend an additional $172 billion on gasoline alone.

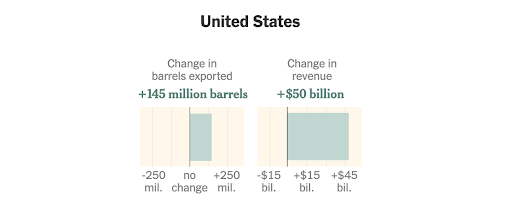

At the same time, the economic effects of an oil shock are very uneven. While consumers struggle, oil companies and investors profit from higher prices. Both major and small oil companies reported huge increases in free cash flow during the first quarter, while the S&P 500 energy sector has experienced a 32% gain this year. Higher oil prices are also boosting tax revenues in oil-producing states like Texas, Alaska, and North Dakota.

This oil boom looks very different from the previous decade's. Despite soaring profits, there is little evidence that oil companies plan to expand drilling or increase their workforce. Improvements in drilling technology allow companies to produce more oil with fewer employees, and many firms seem more focused on investor returns than expanding production. According to the Labor Department, employment in oil and gas extraction is near its lowest level since 1972, and the number of oil rigs has fallen by 11% over the past year.

Meanwhile, many lower-income Americans are already feeling the strain of rising energy prices. As gas prices rose in March, households earning less than $125,000 reduced their gas purchases, while wealthier households barely changed their behavior. Economists believe wealthier Americans have been better able to absorb higher energy costs because their wealth has grown exponentially since 2022. Businesses that rely on lower-income consumers, including fast-food chains and pawnshops, have already noticed weaker customer spending.

The oil shock has created a difficult tradeoff for the Fed. Weakening economic growth would normally encourage the Fed to lower interest rates. But persistent inflation may force policymakers to keep rates elevated for longer to prevent prices from rising further. Consumer inflation expectations increased from 3.8% in March to 4.7% in April, raising concerns that inflation could become harder to control. Chicago Fed President Austan Goolsbee recently described the situation as increasingly resembling an “inflationary shock,” or inflation caused by disruptions in supply rather than strong consumer demand, which is much more difficult to manage.

The Iran war has revealed how vulnerable the global economy still is to disruptions in energy markets, despite years of investment in renewable energy. Even if the conflict eventually de-escalates, uncertainty surrounding global energy supplies may keep prices elevated for months. Although the world looks very different from it did during previous oil crises, the global economy remains heavily dependent on oil.