The Match that Lit the Fire: Volatility in Emerging Markets

On the morning of February 28th, 2026, the United States and Israel launched nearly 900 strikes on Iranian Soil targeting missile silos, air defenses, military infrastructure, and leadership. By the time the markets opened in Asia, traders weren’t just pricing in a war, but rushing to cover their more risky positions.

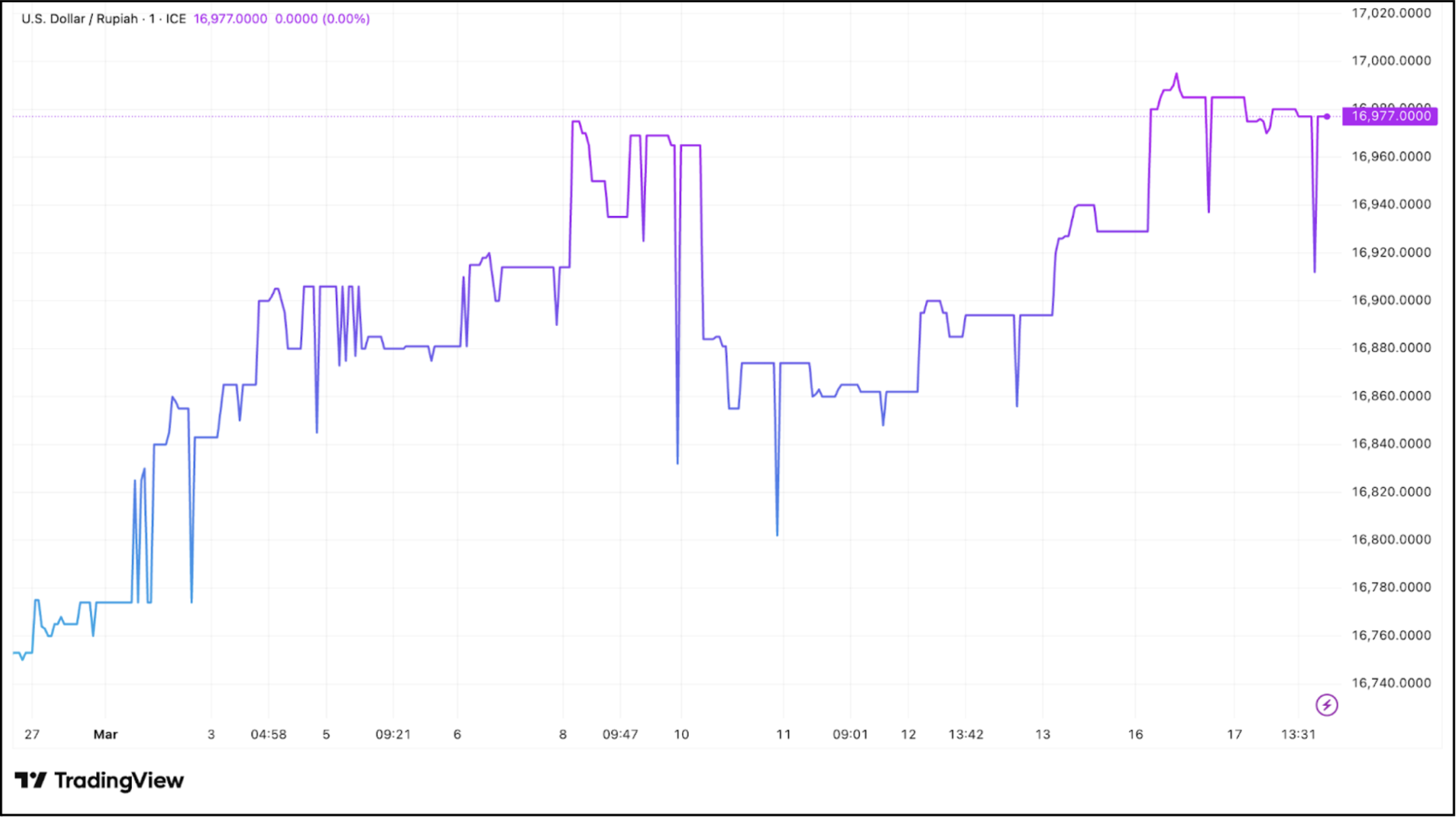

On March 3rd in Jakarta, the Indonesian Rupiah surpassed 17,000 per U.S. dollar, a level not seen since the Asian financial crisis of 1998. The Jakarta Composite Index (Indonesia’s S&P) fell by more than 5% in a single session. This type of volatility can make a Forex trading floor go berserk. But let's be clear, Iranian troops and tanks are not rolling onto pink beaches in Bali. The conflict in the Middle East is exacerbating cracks that were already there.

An Electronic board at the Indonesian Stock Exchange in Jakarta (Bloomberg)

A Tinder Box

The president of Indonesia, Subianto Prabowo, campaigned on a ‘risky’ economic policy during a period of a shrinking middle class when he took office in 2024. MSCI has also recently released a warning about monopolistic behavior in the markets. Then, weeks before the first strike of “Epic Fury," President Prabowo nominated his own nephew to the central bank’s board. Investors viewed this as an immediate threat to monetary independence and divested further. The currency began sliding, and the Bank of Indonesia intervened in the currency markets, buying bonds to try to stem the slide.

Then, the conflict thousands of miles away hit. Indonesia—a country that imports a third of its crude oil and gas from the Middle East—now has to spend trillions of Rupiah more to cover the supply drop; sparking escalating price pressures.

The news coverage of Iran often focuses on direct participants, the Strait of Hormuz, and U.S. or European interests. And while that all matters, emerging markets and people in impoverished countries are experiencing rapid inflation and the total loss of spending power. Turkey’s Lira, India and Pakistan's Rupee, and even the South African Rand all tell the same story: structural vulnerabilities and exposure. A year-long rally for emerging markets has come to an end.

USD/IDR (Trading View)

Irony of Dollar Dominance

For years, analysts have predicted de-dollarization in a multipolar world and massive shifts into the yuan or euro. President Trump’s agenda clearly prioritizes accelerating the devaluation to boost domestic spending and exports. However, as soon as a Middle East conflict began, everyone ran back to the dollar, a traditional safe-haven trade. The dollar index (DXY) even hit a one-month high.

U.S. energy independence means that the dollar doesn’t fall when oil spikes, even during a conflict that the U.S. started. In a crisis, people buy what they trust (reserve currencies) rather than focusing on long-term deterioration.

What’s the Path Ahead?

Cargo Ship observed by the Iranian IRGC (CNBC)

Many third-world countries and general oil importers that are experiencing rapid devaluation will remain exposed to the Middle East until the Strait of Hormuz reopens. Central banks are running low on the tools used to keep their buying power in check. Various states could be forced into unfavorable trade deals for crucial natural resources. Some investors might argue that emerging and exotic markets are in a “buy-on-the-dip” scenario. However, amid increased speculation about a prolonged conflict, fundamental concerns will likely grow as these sensitive economies absorb the shocks from commodity markets. Systemic disruption will cause sustained volatility.

Currency “Winners”:

🇺🇸 USD — energy independent, safe haven, EM capital fled back to dollar

🇯🇵 JPY — classic currency safe haven

🇨🇭 CHF — Swiss neutrality = demand spike every crisis

🇮🇱 ILS — markets priced in Israeli victory, risk premium collapsed

🇸🇦 SAR — pegged to dollar, oil revenues surging

🇳🇴 NOK — Brent spike = Norwegian windfall

Currency “Losers”:

🇮🇩 IDR — 1998-level lows, two simultaneous crises before conflict even started

🇹🇷 TRY — structurally broken, CB intervention a band-aid

🇮🇳 INR — oil import dependency turned conflict into currency event

🇵🇰 PKR — IMF bailout, near-zero reserve buffer

🇪🇺 EUR — energy import dependency, weakened as oil climbed

🇮🇷 IRR — 1.75 million per dollar, down 30% since January, not internationally tradeable