The Cut That Isn’t Coming

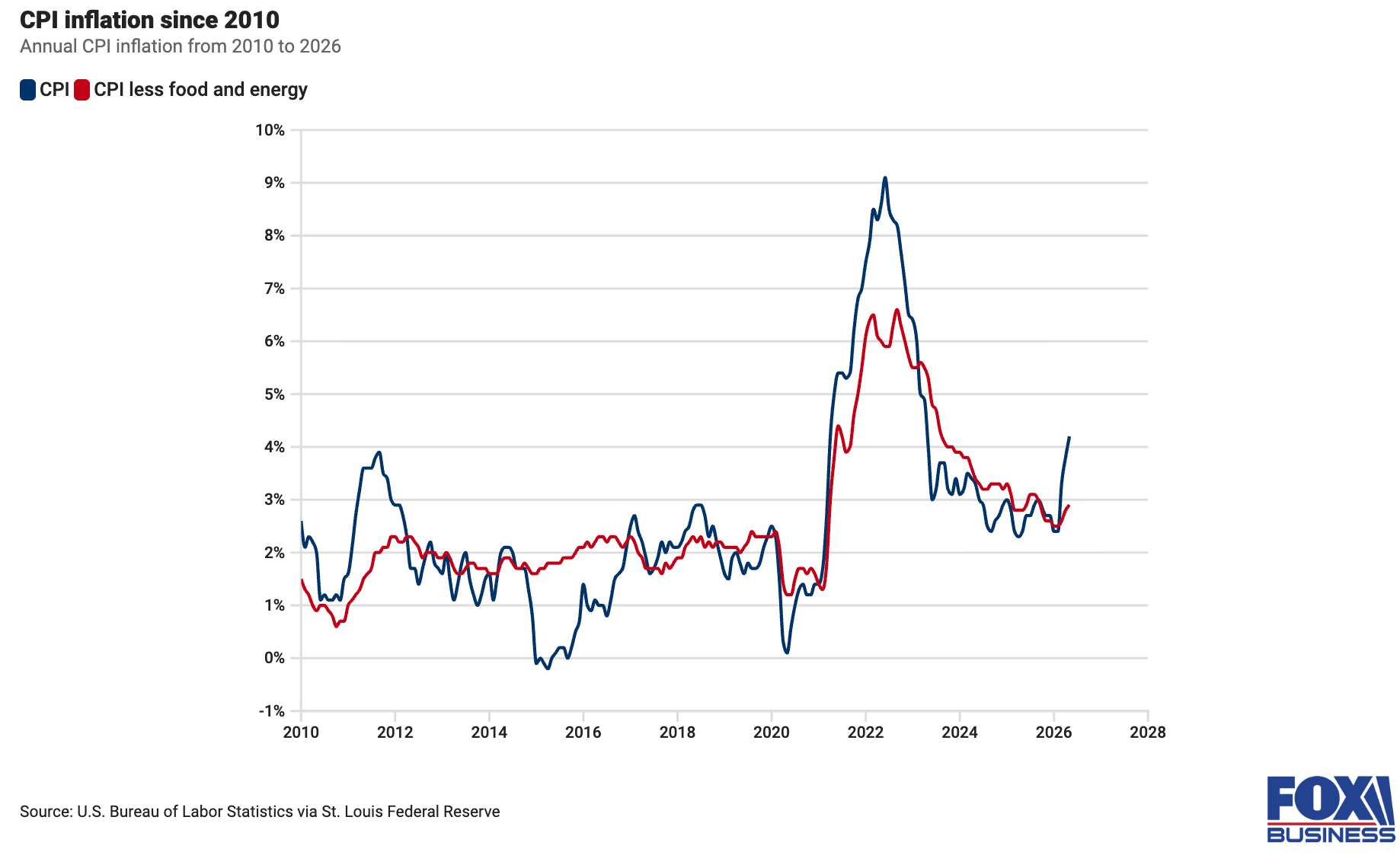

A month ago, the debate was about how many times the Fed would cut interest rates this year. May’s inflation report flipped that question on its head. Consumer prices rose 4.2% year-over-year, the highest rate in three years, and 0.5% month-over-month.

What makes the report complicated is that the 4.2% figure overstates how broad the problem actually is, since almost all of the increase came from energy. Energy prices rose by 3.9% in May and are up 23.5% over the past 12 months, and they accounted for more than 60% of the overall increase this month. On the other hand, core CPI, which excludes food and energy and is used to gauge the underlying trend, rose just 0.2% for the month and 2.9% over the year. While core inflation has barely budged, the headline rate has increased from 2.4% in January to 4.2% in May, almost entirely because of oil.

Shelter, which makes up over one-third of the index and has been one of the most stubborn drivers of inflation since 2022, tells the same story. In May, it rose by only 0.3%, half the increase in the previous month. Shelter is slow to move, so even a small slowdown suggests the trend is real rather than temporary. But this is not what is driving the headline number, and the trouble for the Fed is that it cannot do much to slow this kind of inflation. Energy prices are rising because of a war, not because of demand, and higher interest rates do not bring oil prices down.

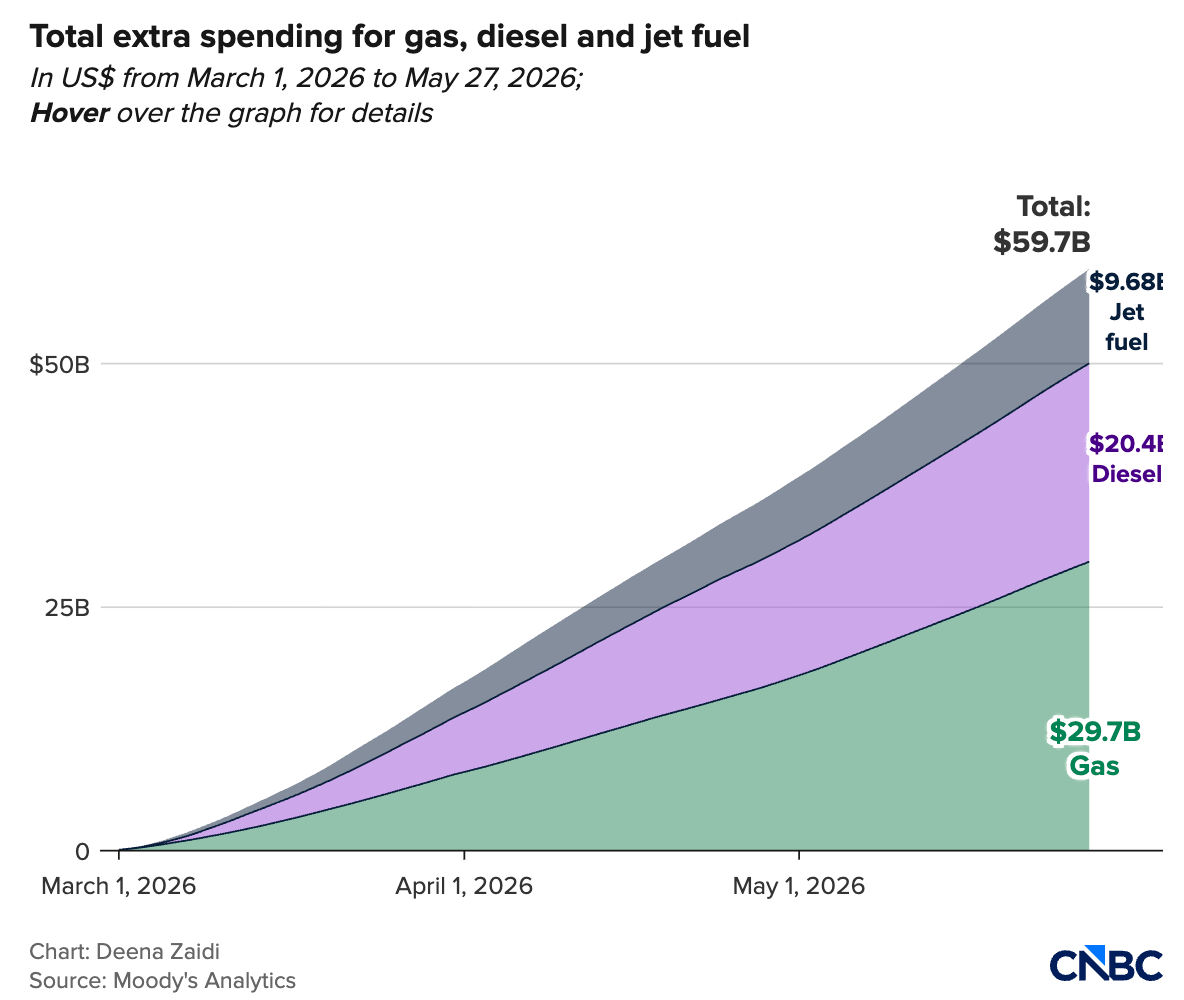

None of that makes the increase any less painful for households. Gas prices rose 7% in May alone and are now up more than 40% from a year ago. Since the war in Iran began, the average American household has spent about $450 more on gas and energy.

Economists were divided on how worried to be. Some argued the report looked better than the headline rate suggested. Outside the categories affected by the war, there were signs of relief, as prices for new vehicles, furniture, and prescription drugs fell for the first time in over a year. Several analysts said May could represent the peak of inflation this year, while others were more cautious. “Inflation is painfully high,” said Mark Zandi, chief economist at Moody’s, who noted that even if prices are peaking, the current inflation rate is double the Fed’s 2% target and may not return to that level until next year.

The Fed is expected to hold rates steady at next week’s meeting. The bigger question is what comes next. The rate cut that looked likely just a few weeks ago is off the table, and a rate hike is now expected before the end of 2026. When that happens depends largely on the war, since the pressure on prices comes from oil, which is outside the Fed’s control.