Stock Pick of the Week (3/23)

Overview

This week's pick is TransDigm Group (TDG), an Ohio-based industrials company that makes highly engineered components for commercial and defense aircraft. About 75% of its revenue comes from proprietary, sole-source parts, meaning airlines and operators have no choice but to buy from TransDigm to keep their planes in the air. The real engine of the business is the aftermarket. Once a TransDigm part is installed on an aircraft, it must be replaced repeatedly over the plane's lifetime, which can span 20 to 30 years. That locked-in and recurring demand is what drives the company's pricing power, its industry-leading margins, and its remarkably consistent free cash flow. Layer in a meaningful defense business backed by long-term government contracts, and it is clear that TransDigm is a company that's built to perform in almost any environment.

Drivers

Pricing Power

One of TransDigm's most durable advantages is its ability to raise prices, and then get away with it. Since so many of its components are sole-sourced and FAA-certified, switching to a competitor isn't just annoying, it's often effectively impossible. Airlines and defense contractors need parts constantly; only TransDigm makes those parts, and recertifying from an alternative company can take years and cost millions. That dynamic gives TransDigm a level of pricing control rarely seen in manufacturing, and it shows up directly in the margins.

Acquistions

The company targets small, niche aerospace suppliers with proprietary (custom) products, acquires them at reasonable prices, and then brings them into their playbook to expand margins and unlock value. It's basically a private equity model operating within a public company. What makes this particularly compelling is the runway ahead: the aerospace component market remains highly fragmented, meaning there's no shortage of acquisition targets, and many more companies for TransDigm to acquire within regulations.

Defense Exposure

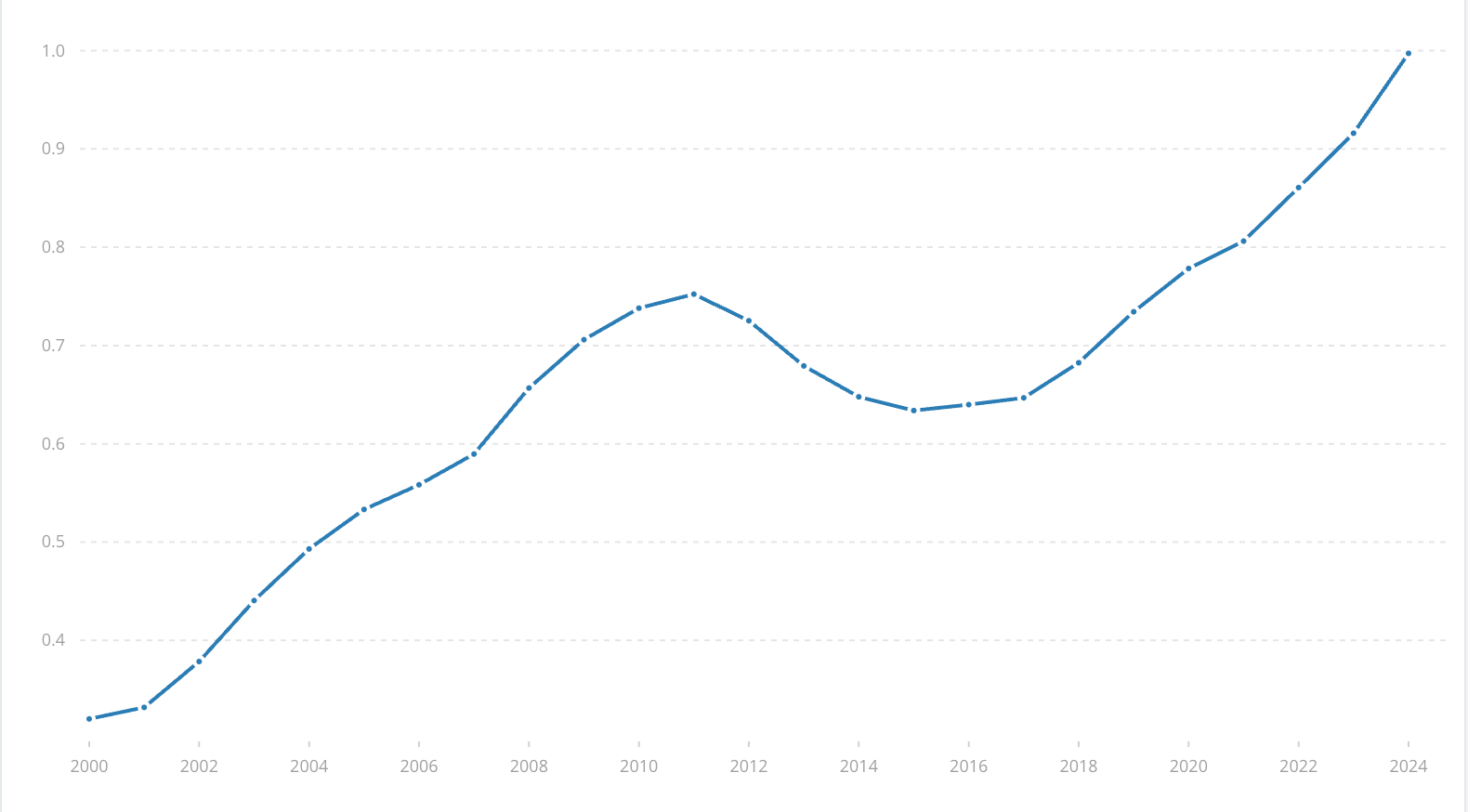

TransDigm's commercial aerospace business gets most of the attention, but its defense exposure is a quietly important engine that is very important to the story. With rising global defense budgets (see below), driven by increasing geopolitical tensions, countries are shifting into larger, longer military aircraft programs, with TransDigm at the helm of many of them. These contracts tend to be long-duration and very sticky, providing a stable revenue base that cushions the company when cyclicality turns down. It's a natural hedge built into the model: even if leisure travel slows, defense spending rarely will.

US Defense Spending ($T) since 2000

Risks

The primary risk to TransDigm is a downturn in airline demand, which could reduce flight hours and slow replacement cycles. However, most of TransDigm's profit comes from mission-critical aftermarket parts that must be replaced regardless of new aircraft orders, making revenue more resilient than it might appear. Regulatory scrutiny of pricing is another consideration, though the highly engineered and certified nature of its components leaves little room for substitutes, limiting that exposure.

The Financials

TransDigm has quietly built, without a doubt, one of the most impressive financial profiles in the industrial sector. The company brought in nearly $8.8 billion in revenue in its most recent fiscal year, up about 11% from the year before, and expects to grow that to roughly $9.75–$9.95 billion in fiscal 2026. However, what really turns heads is the profitability. TransDigm consistently converts more than half of its revenue into EBITDA (earnings before taxes, interest, depreciation, and amortization), a margin most manufacturers can only dream of. They have generated $4.5 billion in EBITDA last year and over $1.8 billion in free cash flow. The company also returned an eye-popping $5.8 billion to shareholders last year through special dividends and buybacks, a sign of just how much cash the business generates and of the management's confidence.

Why-to-Buy

At TransDigm’s core, it is a business built to win. They dominate manufacturing highly specialized, hard-to-replace aerospace components. The company has spent decades acquiring niche aerospace businesses and pushing out exceptional returns.

Planes aren't going anywhere, air travel demand continues to climb globally, and aircrafts need TransDigm's parts to keep them off the ground. The financials back it all up: high margins, consistent double-digit growth, and billions returned to shareholders YoY.

For long-term investors, TDG offers a rare combination: a defensive, recession-resistant business with the growth profile of something far more exciting. In a market full of uncertainty, TransDigm is the rare pick that should earn a spot in any portfolio.