Fed Policy Transition and Geopolitical Risk

This week, the global macroeconomy was driven by three things: the debut of Federal Reserve Chair Kevin Warsh at his first FOMC meeting, the U.S.-Iran peace negotiations, and continued uncertainty over inflation.

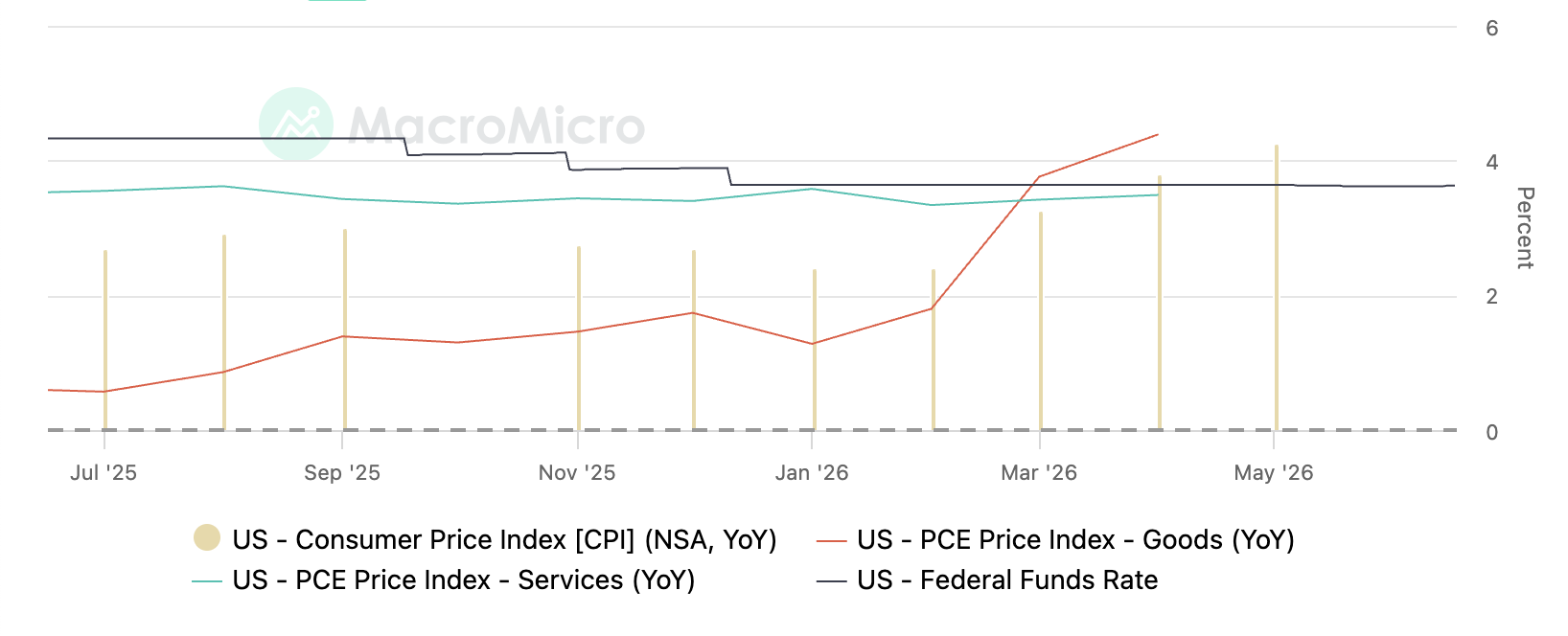

The Federal Reserve held rates steady during Kevin Warsh’s first meeting as chair. Markets expected this decision, but investors paid close attention to what Warsh prioritized. He emphasized a renewed focus on price stability and signaled that the Fed would provide less forward guidance than in previous years, creating a potentially less predictable monetary policy environment.

This approach is significantly different from former Chair Jerome Powell’s emphasis on transparency. Warsh announced several task forces to reevaluate the Fed’s communication strategy, balance sheet management, inflation targeting, and productivity measurement. The markets interpreted his remarks as slightly hawkish, increasing expectations that additional rate hikes may still occur later this year if inflation remains elevated.

U.S. inflation measures and the Federal Funds Rate, July 2025–May 2026.

Another important event this week was the release of economic data by the U.S. government. Consumer spending has remained somewhat resilient, but business investment has shown signs of slowing. Labor markets are also beginning to slow, with job openings declining and hiring becoming more selective across several industries. These create difficult decisions for policymakers because a slowing economy would justify lower interest rates, but persistent inflation prevents the Fed from easing monetary policy too quickly, putting them in a tough spot to carry out the dual mandate.

Geopolitics also heavily influenced attitudes towards the market. Earlier this week, the White House submitted an agreement with Iran to Congress after both countries signed a deal establishing a temporary de-escalation framework. Under the agreement, the U.S. would slowly lift certain restrictions, while Iran would guarantee commercial passage through the Strait of Hormuz for a 60-day period while both sides negotiate a permanent arrangement, likely having to do with nuclear weapons. However, the situation remains fragile. Planned follow-up talks in Switzerland were postponed due to renewed fighting involving Israel and Hezbollah in Lebanon.

From a macroeconomic perspective, the success or failure of these negotiations will have enormous implications. A lasting agreement would reduce oil prices, stabilize global energy markets, and ease inflationary pressures worldwide. Conversely, a breakdown in negotiations could reignite supply chain concerns in the Middle East and put upward pressure on gas prices and headline inflation.

Overall, the economy enters the second half of 2026 in a tough spot. Inflation remains above target, growth is slowing, and central banks are navigating an uncertain geopolitical environment. Investors are now balancing optimism surrounding de-escalation in the Middle East with caution regarding tighter monetary policy under Warsh’s leadership. The coming months will depend on whether negotiations evolve into an actual agreement and whether inflation will slow enough for the Fed to avoid additional rate increases.