Is the Clock Ticking on the World's Biggest Borrowing System?

For decades, this financial strategy quietly pumped cheap money into global markets. Now, the engine is powering down.

The system begins by borrowing at nearly zero percent interest, converting the funds into dollars, and investing in assets that pay roughly 5 percent. Pocket the difference, and repeat at scale. For years, this was the basic structure of the Yen Carry Trade, quietly powering global markets.

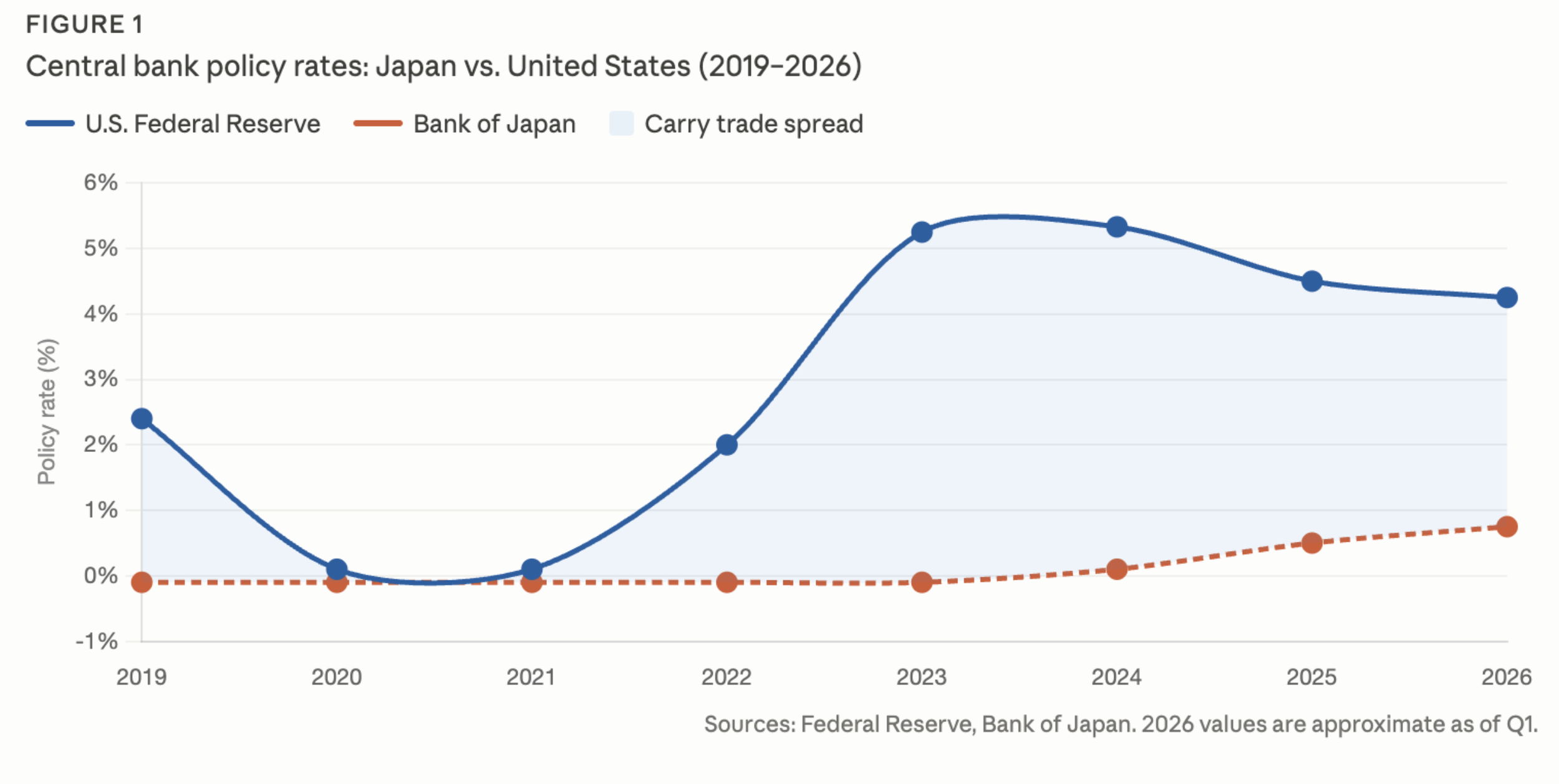

The strategy worked because the Bank of Japan (BOJ) held interest rates near or below zero for decades while the rest of the world (especially the United States) kept rates higher, often aiming to curb inflation. That gap between these interest rates is lucrative — but as of 2026, that gap is tightening significantly.

Central bank policy rates — Japan vs. United States (2019–2026). Production of charts assisted by Claude.

Why It's Ending

The BOJ has quietly begun raising interest rates, representing a historic shift after years of keeping them at zero or even negative. Meanwhile, the U.S. Federal Reserve has, by and large, been moving toward rate cuts. Despite being beset by inflationary pressures because of the Iran situation, the long-term strategy still appears to be the eventual slashing of rates. Additionally, with Kevin Warsh at the helm of the Fed, a more aggressive stance on cuts may follow. The result is a narrowing spread for the carry trade. When this gap shrinks, the profit disappears, and the trade loses its mathematical rationale.

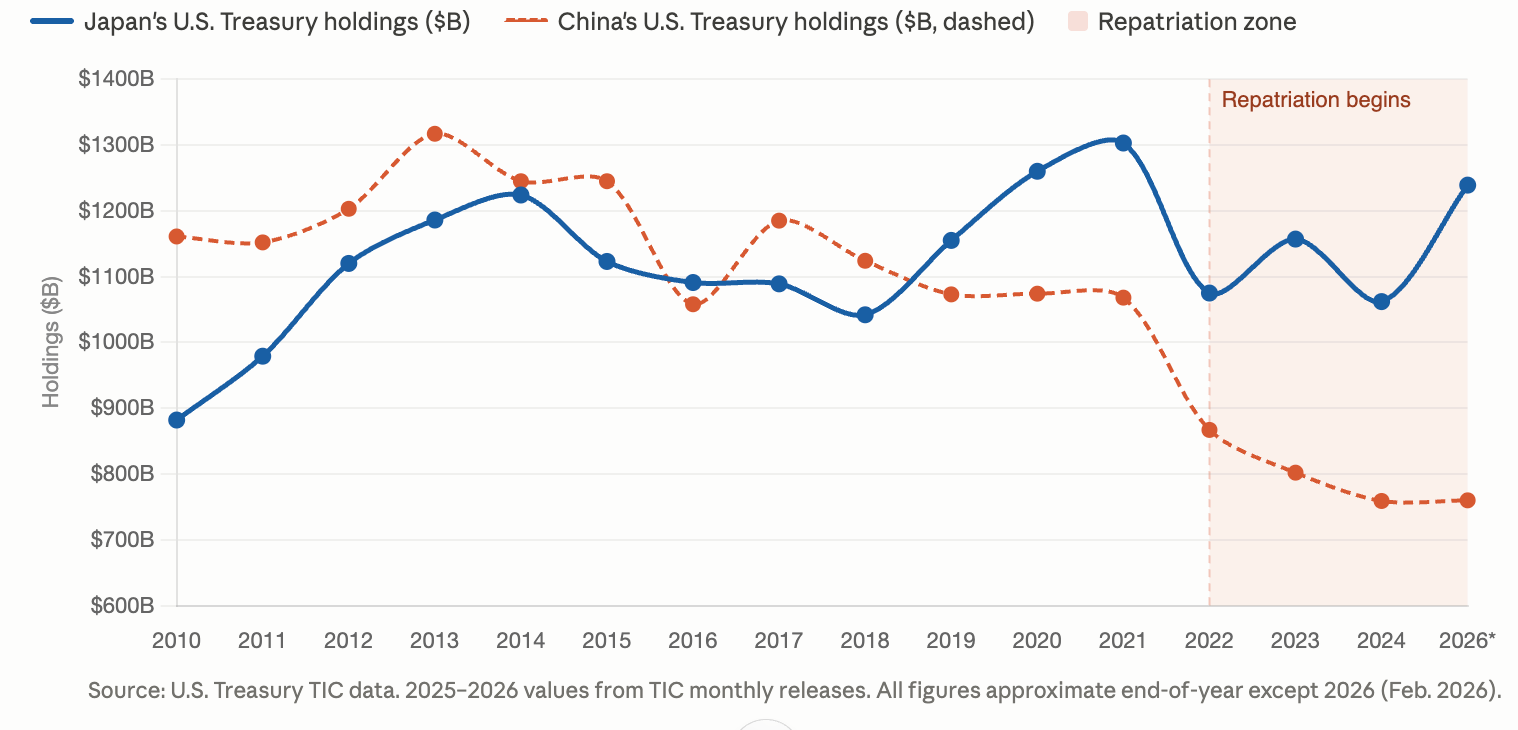

At the same time, Japanese government bonds are offering yields not seen in decades. That gives Japan's biggest institutional investors, such as pension funds and insurers, a compelling reason to bring their money home rather than invest in U.S. Treasuries. This is called capital repatriation, and it means consistent, large-scale buyers of American debt are quietly stepping back.

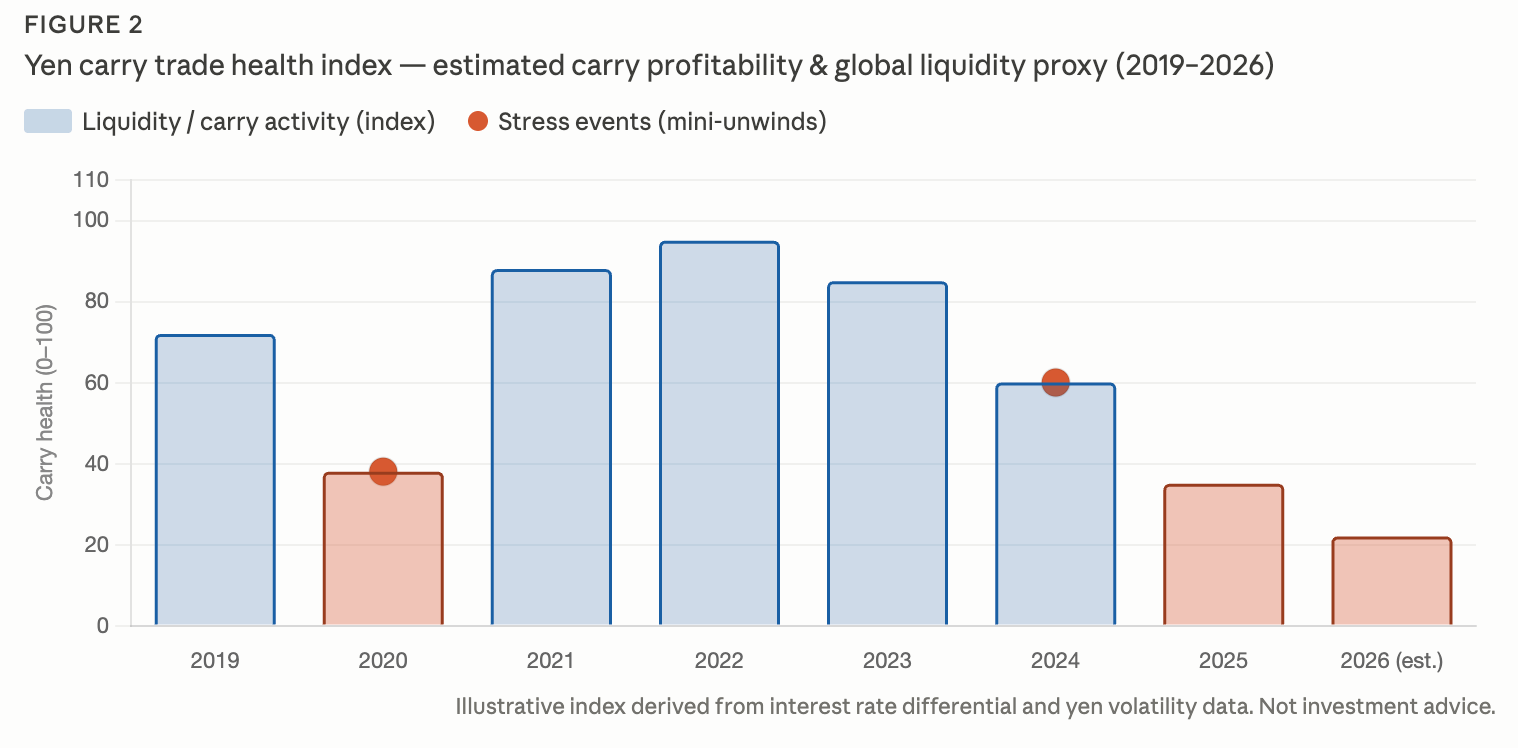

Yen carry trade health index (2019–2026). Index combining rate differential and yen volatility data, showing steady post-COVID decline. Production of charts assisted by Claude.

What Happens When it Unwinds

So what happens when investors close their carry trade positions? They sell U.S. assets to buy back yen and repay loans. That selling pushes U.S. bond prices down and yields up, making government borrowing more expensive. TD Economics estimates this dynamic could add 20 to 50 basis points to the U.S. 10-year yield in the medium term. And at a large scale, it can trigger sharp sell-offs in stocks, since a lot of that cheap yen flowed into equity markets.

What we are really seeing is risk accumulation without a full escalation, as the trade has contracted, but hasn't collapsed. But what makes it dangerous is its sensitivity to shocks. Even small policy announcements from the BOJ have triggered sudden yen spikes and mini-unwinds in recent months, a warning sign that the underlying structure is over-leveraged (BIS).

Japan's holdings plateaued and have started declining as a share of total U.S. debt. In fact, total Treasury debt outstanding grew from $20.9 trillion in 2020 to $28.1 trillion by the end of 2024, but foreign holdings increased by only $1.2 trillion over that same period, meaning foreigners' share of U.S. debt has actually been shrinking. (Congress.gov)

Who Wins, and Who Loses?

First, value investors stand to benefit. As cheap capital recedes, markets begin rewarding cash flow and profitability over speculative growth. Japanese households also benefit, as this shift in capital supports domestic markets and raises purchasing power.

On the other hand, the U.S. Treasury faces a structural problem: it must offer higher yields to attract buyers as a major source of foreign demand quietly exits, first from China and now from Japan. Highly leveraged hedge funds are the most immediately exposed, as yen spikes trigger margin calls and force them to liquidate even high-quality positions first.

Why This Matters Beyond Finance

The Federal Reserve's ability to steer the economy is constrained by these global flows. If the Fed cuts rates to stimulate growth but the dollar weakens too quickly as foreign capital retreats, it risks stoking inflation and financial instability. The carry trade has, in other words, quietly shaped U.S. domestic policy for years.

Economists describe Japanese capital as a "critical anchor" that held global interest rates lower than they would otherwise have been. As that anchor lifts, borrowing costs for everything, such as mortgages, corporate bonds, and government debt, will become more exposed to global volatility.

Ultimately, the era of cheap money powered by the yen carry trade is not ending in a single crash, but it is deflating slowly. The winners in what comes next will be those who build for a world where capital is no longer free. Or, they will be forced to find another way to make it free.