The Body as a Balance Sheet: Screenless Wearables and the Subscription Health Bet

For most of modern medicine, the annual physical was the apex of personal health data: a resting heart rate, a blood pressure reading, and a chart note filed for another year. That snapshot model is now colliding with a new consumer paradigm - one in which people are financing its disruption themselves, $6 a month at a time.

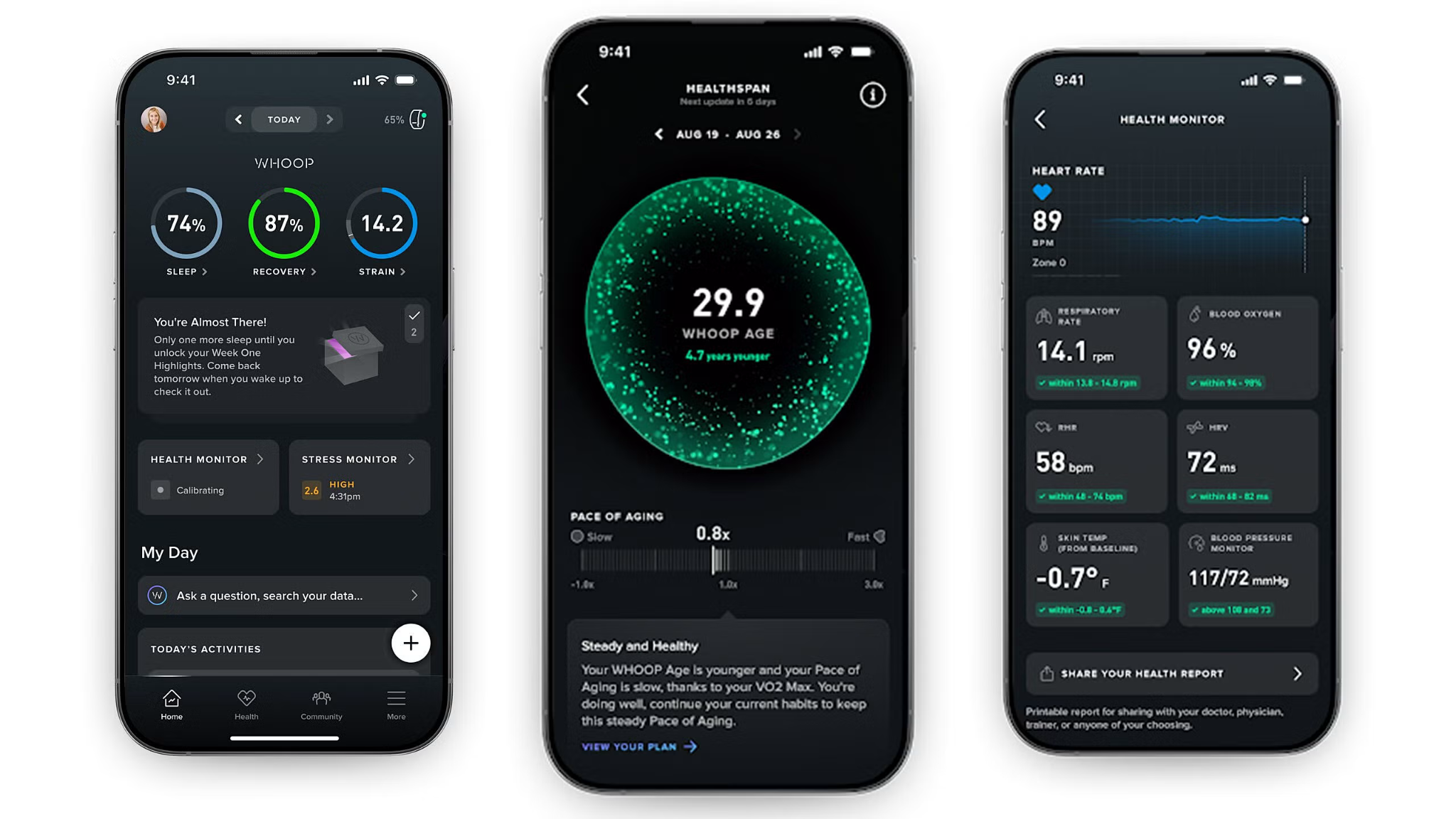

The screenless wearable sector, led by Oura Health and Whoop, has, in roughly 24 months, gone from biohacker novelty to an institutional investment magnet. Both companies crossed $1 billion in annualized revenue in 2025 and now carry private valuations above $10 billion each - a territory that would make them meaningful entrants in the S&P 500 health care sector if they were public.

The Subscription Flywheel

The hardware-plus-subscription model that briefly made Peloton famous is being executed with considerably more discipline here. Oura sells its ring for $349 and up, then charges $6 a month for the analytics platform that makes the hardware valuable. By Sacra Research's estimates, Oura generated approximately $1 billion in total revenue in 2025, doubling its 2024 performance, with roughly 80% attributable to hardware and 20% to recurring subscriptions. That mix matters: hardware revenue is lumpy and capital-intensive, while subscription revenue is predictable and margin-expanding at scale.

Whoop inverts the model entirely, bundling hardware into an annual membership priced between $199 and $359 - more analogous to a software subscription that ships a device. The company reported 2.5 million members, 103% year-over-year subscription growth, and a $1.1 billion revenue run rate heading into 2026. Perhaps most significantly for institutional observers, Whoop also turned cash-flow positive in 2025, separating it from the cohort of growth-at-any-cost health tech firms that collapsed between 2021 and 2023.

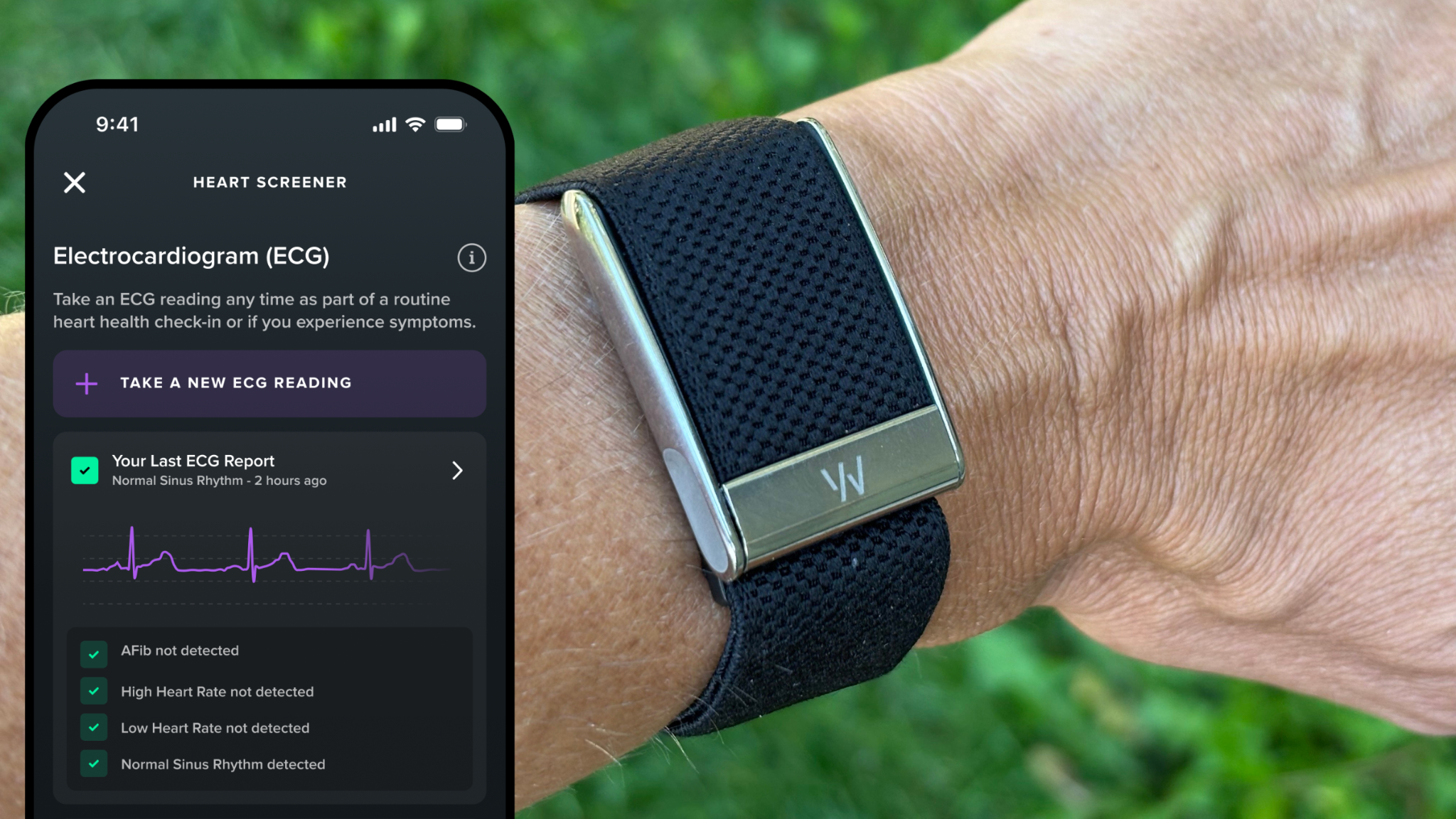

Both companies are now layering laboratory diagnostics onto their platforms - a move that could expand average revenue per user substantially. Oura's partnership with Quest Diagnostics allows members to schedule blood draws and view 50 biomarkers alongside ring data. Whoop's Advanced Labs panels offer tiered blood testing from $199 to $599 per panel. These services transform each company from a sensor manufacturer into a longitudinal health data platform, a positioning that commands a fundamentally different valuation multiple.

Market Structure

The smart ring category is young enough that market-size estimates vary across research providers, but the directional consensus is tight. Grand View Research pegs the 2025 market at $417.5 million, projecting growth to $2.1 billion by 2033 at a 22.5% CAGR. Shipment data from Omdia provides the clearest unit view: global smart ring shipments exceeded 850,000 in 2023, more than doubled to 1.8 million in 2024, and are tracking toward 4 million units for full-year 2025. U.S. consumer purchase data from Circana shows that smart ring purchases grew 195% between 2024 and 2025, and broader fitness tracker purchases grew 88%.

Within that market, Oura's position is unusually dominant. The Finnish company controls approximately 74% of smart ring shipments as of H1 2025, followed by Ultrahuman and Samsung at roughly 9% each. That concentration provides pricing power and data-network advantages - more users generate richer longitudinal datasets, which improve algorithmic accuracy, which attract more users. But it also makes the company a primary target as platform giants enter the category.

The most immediate structural threat is the subscription-free alternative. Both Ultrahuman and RingConn have explicitly positioned themselves against Oura's recurring fee model, offering comparable hardware as one-time purchases. Oura's response has been legal rather than price-competitive: the company secured International Trade Commission exclusion orders against both competitors in 2025, effectively banning their infringing devices from the U.S. market, while reaching royalty-generating licensing agreements. A $250 million revolving credit facility arranged by JPMorgan, Goldman Sachs, and Bank of America backstops the longer platform play.

The Valuation Question

At $10–11 billion, both companies trade at roughly 10 times trailing revenue - a multiple that prices in substantial continued growth. Garmin, the most comparable public company by product mix, trades at approximately 3–5 times revenue. The premium Oura and Whoop command reflects a software company framing: if subscriptions grow to 40–50% of revenue, the blended multiple becomes more defensible. But that transition is not guaranteed.

Subscription growth has a ceiling that hardware growth does not. Oura's addressable subscriber base is bounded by ring sales, which in turn are bounded by consumer willingness to pay $349–$499 upfront. Maveron's Consumer 2026 report suggests one in three U.S. adults will own a health wearable by year-end - a penetration level that begins to raise real saturation questions. Meanwhile, Samsung and Google have entered the category with devices that carry no subscription fees, leveraging existing platform trust and ecosystem lock-in.

The most credible upside, conversely, lies in reimbursement. Whoop's selection into the CMS Innovation Center ACCESS program, launching July 2026, will enable Medicare beneficiaries to access Whoop's platform through a reimbursed care pathway - a structurally new distribution channel that bypasses consumer acquisition costs and reaches tens of millions of chronic-condition patients. If that pathway scales, it would represent a fundamental expansion of the addressable market beyond the athlete and wellness-enthusiast demographics that built both companies.

Outlook

The secular tailwind is genuine. An aging population with rising chronic-disease burden, post-pandemic health awareness, and an overtaxed clinical system all point toward sustained consumer investment in continuous monitoring. HSA/FSA eligibility for both Oura and Whoop memberships, active corporate wellness integration, and the nascent Medicare reimbursement channel represent demand vectors that did not exist three years ago.

The risk is execution, not market. Both companies face the same transition challenge: moving from health reporting to health intervention. A platform that tells you your heart rate variability declined is a useful sensor; one that prescribes a recovery protocol, adjusts training load, and coordinates with a physician is a health operating system. The capital has been raised, and the subscriber bases are large enough to generate meaningful longitudinal data. Whether Oura and Whoop build toward that future - or plateau as elegant sensors at unsustainable multiples - will determine whether their $10 billion valuations prove prescient or premature.