From Crisis to Constraint: The Real Estate Market

Over the past one and a half decades, the U.S. housing market has undergone a dramatic transformation, evolving through cycles of recovery, expansion, distortion, and constraint. By examining these four distinct periods, this analysis highlights how the housing market has transitioned from post-crisis recovery to a structurally constrained system, offering insight into both its recent behavior and its future trajectory.

The Recovery Era, from 2010 to 2015, marked the market's recovery from the 2008 housing crisis. This period is marked by the aftermath of the 2010-2011 crisis, with foreclosures and falling prices; 2012-2013 was the turning point, with demand returning and prices rising; and finally, 2014-2015 showed stabilization and a gradual return to normal.

The expansion phase, marked by a healthy bull market, spanned from 2015 to 2019. As the broader economy strengthened and recovered, job growth improved, wages rose, and interest rates remained historically low. Demand returned and steadily increased, pushing home prices up sustainably. Over these 5 years, home prices increased at a consistent 5% annually. This reflected a balanced market supported by economic growth.

The pandemic boom from 2020 to 2022 altered the housing market's trajectory, driven by an unprecedented surge in demand. This demand can be attributed to interest rates being slashed to promote economic growth, remote work reshaping housing preferences, and fiscal stimulus checks that boosted household savings. Home prices rose into double digits in some areas, and bidding wars over the asking price became common. Buyers were aggressively competing for limited inventory, and in two years, the prices accelerated at a pace that would normally take a decade.

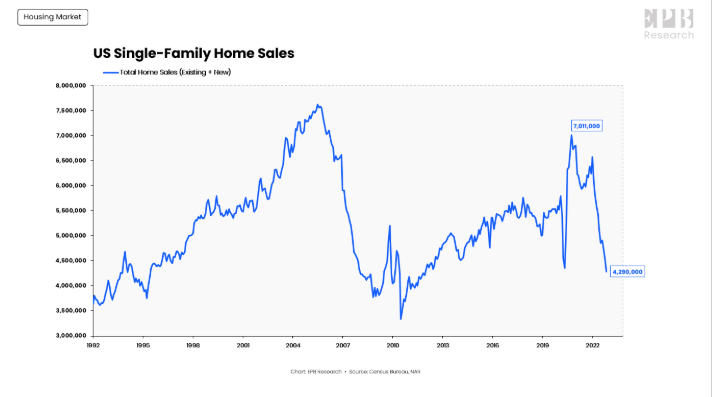

Finally, from 2023 to 2025, we saw inflation surge following the COVID-19 pandemic, while interest rates rose. Mortgage rates climbed drastically, affecting affordability and pricing any buyers out of the market. However, even with this increase, home prices did not collapse. Instead, the market stagnated, transactions slowed, listings declined, and on both ends, buyers and sellers stepped back. A key factor in this period is that many homeowners secured ultra-low mortgage rates during the pandemic and are now unwilling to sell, even as borrowing costs have risen. The result is a constrained market characterized by high prices, low transaction volume, and low inventory.

Over the past 15 years, real estate has moved through three distinct phases: recovery, expansion, and distortion. Today, it enters a fourth phase of constraint. The next decade will not deliver the extraordinary gains of the past, but it will reinforce housing as one of the most structurally supported asset classes. With supply limited, demand persistent, and affordability stretched, the market is unlikely to experience dramatic declines. Instead, real estate will settle into a new role: slower, steadier, and more dependent on fundamentals.